- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 8, 2021 at 11:15 am

A bi-weekly publication dedicated to the principle that deeper and broader knowledge drives superior investment results.

There are two reasons why you should care about the ongoing meltdown of China’s overindebted property developers. The first is that, in my opinion, these debt-driven companies are at far greater risk of extreme financial distress than consensus currently expects. The second, is that their weakness threatens to spread into other markets globally. After all, there is a reason that financial distress is often called “contagious.” It leaps from where it started to other previously un-infected markets. Right now, with the U.S. and many other markets ignoring the Chinese meltdown, we think it’s a time for exercising caution. Today, we outline the “Bizarro World” dynamics that are driving China’s property developers and how that could weigh on global asset markets. Our goal in doing so is to set the stage for why you should listen to our recent interview with former Wall Street Journal reporter and author of “China’s Great Wall of Debt” Dinny McMahon (see link at the end of this piece).

The dramatic failure of Evergrande, China’s second largest real estate company with $300 billion in debt is all over the financial news – now. I have been watching this saga unfold for months with interest because Evergrande has long been on my mind. In fact, ten years ago, worried that the next big financial crisis could start in China, I traveled to China to research its debt powered real estate boom. From afar, Evergrande and the ongoing boom eerily resembled the events that preceded the US housing crash, and subsequently, what would come to be known as the Global Financial Crisis. The deeper I dug during my research trip to Wuhan, Changsha, Beijing and Shanghai – the worse it looked.

Is China’s long-running real estate boom (finally) turning into a bust? To answer this question, our research team recently interviewed Dinny McMahon, author of “China’s Great Wall of Debt,” published in 2018. I first met Dinny on my trip to China a decade ago in Beijing. Dinny was a reporter for the Wall Street Journal and had studied China’s financial system for years. Now, a full ten years later, Dinny’s insights are in demand as Evergrande’s woes are splashed all over the front page. My goal here is to set the stage for the insights he shared in our interview – a link to which is at the end of our writing. But you can’t hope to properly understand these events without the proper context. To help explain why I have been so focused on Chinese real estate for the past ten years, you first need to understand that credit driven markets like real estate follow different rules. Today, we explore the strange “Bizarro world” rules of Chinese real estate, and why you should care about it.

We all know the story of Superman. But that of Bizarro, essentially Superman’s evil twin and alter-ego, may be new to many. Bizarro, pictured above, first entered the world of superhero comics in 1958. He was the mirror image and opposite of Superman. Bizarro lived in a strange world that operated by totally opposite rules from that of Superman’s Earth. In Bizarro’s world, good meant bad. Even the shape of Bizarro’s world was different: where the earth was round, Bizarro’s world was a cube. This idea of different rules prevailing on Earth vs. Bizarro world is an important concept to understand if you are going to understand how the rules of real estate are different from what you might otherwise expect.

The normal investment world Earthlings know is almost exclusively linear. Change is slow and incremental. Today looks like yesterday. Tomorrow can be expected to look like today. Mean reversion is the Earthling’s mantra. Assets have a fundamental and intrinsic value. Price mean reverts in small fluctuations around this equilibrium value and rarely strays by much from it. For instance, a stock with an objective fundamental value of $100/share should be bought if its price falls to $50/share, because its undervalued and should rise back to its unchanged, fundamental price of $100. So, the right strategy is to buy low, and sell high. This is value investing 101. Patience is essential to allow enough time for security prices to move to their fundamental value.

Those are Earth’s rules.

Bizarro World works differently. Real estate is a Bizarro World asset because its fluctuations are super-charged by credit flows.

Bizarro World’s rules could be considered as the exact opposite of everything you know here on Earth. On Bizarro World you will find no such thing as unchanged and fundamental intrinsic value. Prices do not revert to equilibrium but rather they accelerate away from equilibrium to extreme highs then are subject to crashing to extreme lows. On Bizarro World, you do not buy low and sell high – the discipline so needed for mean reversion. Rather prices which follow this world’s different rules tend to move away from fair value to extremes. So, to succeed in Bizarro World you need to be ready to do the opposite: you buy high – on the expectation that rising asset prices go higher – and you sell low – on the expectation that falling asset prices go lower. The difference is that asset values on Bizarro world have a much higher odds of boom and bust behavior, of bubbling to shocking highs and crashing to unfathomable lows. Bizarro World assets, like real estate are different. Let me explain…

One reason that Bizarro World assets behave differently is because their prices are debt driven, which gives them a quality that George Soros has called “reflexive.” This means that the act of valuing the asset impacts the value of the asset. Price acts upon the fundamentals. Or, better put, prices are fundamentals. Remember that, in Bizarro World, there is no unchanged “value” or price equilibrium that invariably pulls prices towards it. Rather trends in prices become self-reinforcing because their feedback loop operates strongly back upon the credit market from which they draw their financing. Credit flows can be thought of as bubble fuel. For instance, because real estate prices are high and rising, banks are more willing to loan against this rising collateral value. As this expectation becomes entrenched, such loans seem safer. This creates the paradox that, the more housing prices rise, the more banks are willing to lend, and with more bank lending, prices go a lot higher. Perception becomes reality.

The same self-reinforcing cycle works to the downside, when prices are falling.

Falling real estate prices lead banks and other creditors to conclude that lending against their falling collateral values is risky, so the lending slows. When this expectation becomes entrenched, credit flows collapse and with them transaction volumes. Price can be expected to confirm the downturn in transactions, in time. Then the whole process feeds upon itself. There is no such thing as intrinsic, fundamental value in these markets. For this reason, the most profound capital losses for otherwise disciplined value investors take place in reflexive, Bizarro World markets. Why? Because when a debt fueled bull market reverses, its falling prices supercharge a fast moving, debt powered collapse of potentially shocking speed and depth. The graveyard of value investors is littered with the bleached bones of otherwise savvy investors who mistakenly apply Earth logic to a Bizarro World market. This is an absolutely fatal error. I have seen it many times. This is why I am highlighting this risk now.

But don’t blame the investors who don’t understand these cycles and the creditors who drive these Bizarro World forces.

These investors, like Earthlings, can live 99% of their lives in the confident expectation that our planet’s mean reversion and linear rules will hold. The problem, however, lies in that rare 1% of the time when a reflexive, debt-fueled market transitions from Earth’s rules and enters Bizarro World. Unless you have studied the Dark Arts of Bizarro World (reflexive) markets, its easy to miss the signposts that the old rules no longer apply.

If you are wary, however, you can identify the change. You just need to know where to look.

That’s why our interest in China’s real estate market is so keen at this very early stage of the game. That’s why I went to China ten years ago: to do a deep dive on the Bizarro World of the Chinese real estate market. Not because ten years ago I saw anything imminent in the data that troubled me. No, not at all. But rather because my framework identified that the structure of the Chinese real estate market was inherently reflexive – meaning heavily credit dependent. Thus, it would be rational to expect it to exhibit extreme price action – a huge bull market and a resounding collapse. Under the right circumstances, this debt fueled market could turn reflexive as falling credit flows self-reinforced a nascent downcycle into Bizarro world – with devastating consequences.

This may be unfolding right now in China.

Is now the time, after a decade of watching and waiting, for the Chinese real estate market to enter Bizarro World? I think the answer may be yes. If so, investors who mistakenly apply the wrong rules – rules more appropriate for Earth but devastatingly misapplied to Bizarro World – may misjudge how extreme prices may become as the “fundamental value” of real estate in China drops far away from supposedly equilibrium prices at an accelerating rate. Furthermore, given the $60 trillion invested in Chinese real estate, one of the world’s largest asset classes, such reflexive distress could accelerate through China and its multi-trillion-dollar shadow banking system. This opaque web of debt funded the boom and will likely suffer in the bust. We are on the lookout for any eventual spill over impact into the global financial system. Although, to be clear, such a potential event may lie far into the future. My point is this: don’t let it sneak up on you. Educate yourself now and pay attention!

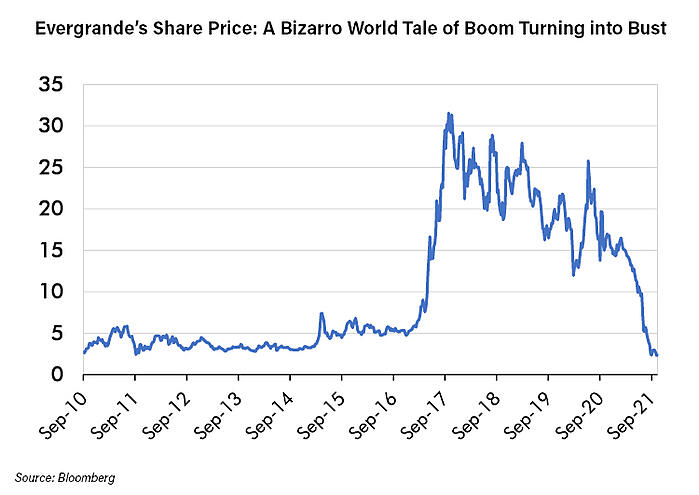

If a picture is worth a thousand words, then surely the amazing boom and resounding bust of the share price of China’s most indebted real estate company Evergrande, must speak volumes (shown below). Evergrande’s volatility has been epic. If you understood that this stock, as a credit sensitive property developer, followed Bizarro World rules then you should have been better prepared to expect the unexpected. A six-fold rally in one year and a 91% decline in 18 months probably wrong footed a lot of smart investors. This is not the kind of thing that happens to “normal” investments. Rather this is exactly what you would expect, however, from a reflexive cycle of credit driven boom and bust.

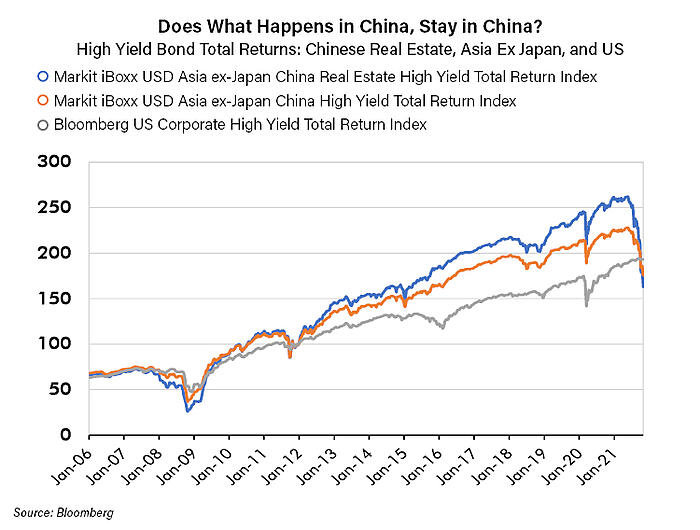

The chart below demonstrates the total return of three high yield bond indices, that of 1.) Chinese Real Estate Developers, 2.) Chinese companies in general, and 3.) A diversified index of U.S. high yield debts. To me, a few things pop out. First, generally the peaks and troughs tend to move together – both US and Chinese together. This makes sense given that the biggest moves in markets tend to be global. Second, today the debts of Chinese real estate companies are collapsing at an incredible pace. Keep in mind that, according to Bloomberg, Chinese real estate company debt now accounts for nearly half (46%) of the world’s dollar denominated distressed high yield debt.

These bonds formerly had been among the world’s leaders in this asset class, now they are collapsing. Furthermore, signs of distress are spreading beyond property developers to infect a more diversified index of Chinese high yield bonds. Will that weakness spread, in time, to the U.S. market? If history is a guide, then the answer would seem to be “yes!”

We believe that one of our most important jobs is risk management. To us, this means looking out for potential future challenges the markets may face. We believe such a serious challenge is now unfolding in the Chinese real estate market. It’s “reflexive” debt-driven dynamics drive a volatile boom and bust cycle that is devastating the price of Chinese property developers and threatens to spread beyond China’s $60 trillion worth of real estate and infect other global markets. We wanted to explain the surprising “Bizarro World” self-reinforcing dynamic at work so that clients and friends could have the proper preparation for hearing the views of Dinny McMahon, the author of “China’s Great Wall of Debt” whom we interviewed at the link below in a special edition of our “Market Happy Hour Series.” We believe that your investment of time to hear his views on this market will be well-rewarded.

—

Originally Posted on November 5, 2021 – The Bizarro World of Chinese Real Estate

CWA Asset Management Group, LLC is an SEC-registered investment adviser, doing business as Capital Wealth Advisors and as blueharbor wealth advisors. CWA’s ADV 2A can be accessed via https://adviserinfo.sec.gov/. This material is as of the date indicated, is not complete, and is subject to change. Any opinions expressed herein represent current opinions only and no representation is made with respect to the accuracy, completeness or timeliness of information and CWA assumes no obligation to update or revise such information. Additional information is available upon request. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified and CWA is not responsible for third-party errors. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Nothing herein should be interpreted as investment advice. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Specific companies or securities described in this report are meant to be illustrative of investment style. Such case studies are not meant to be, and may not be, representative of any portfolio or holdings of CWA Asset Management Group, LLC. CWA does not guarantee the accuracy of information of any third-party website denoted in this article. Third-party website is provided for informational purposes only.

Please note that past performance is not indicative of future results.

This material is solely for informational purposes and is intended only for the named recipient. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision.

CWA Asset Management Group, LLC is an SEC-registered investment adviser, doing business as Capital Wealth Advisors (“CWA”) and as blueharbor wealth advisors. CWA’s ADV 2A can be accessed via https://adviserinfo.sec.gov/. This material is as of the date indicated, is not complete, and is subject to change. Any opinions expressed herein represent current opinions only and no representation is made with respect to the accuracy, completeness or timeliness of information and CWA assumes no obligation to update or revise such information. Additional information is available upon request. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified and CWA is not responsible for third-party errors. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Nothing herein should be interpreted as investment advice. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Specific companies or securities described in this report are meant to be illustrative of investment style. Such case studies are not meant to be, and may not be, representative of any portfolio or holdings of CWA Asset Management Group, LLC. Please note that past performance is not indicative of future results. This material is solely for informational purposes. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision.

CWA does not guarantee the accuracy of information of any third-party website denoted in this article. Third-party website is provided for informational purposes only. CWA is not implying an affiliation, sponsorship, endorsement with/of the third party or that any monitoring is being done by CWA of any information contained within the website. CWA is not responsible for the information contained on a third-party website or the use of or inability to use such site. Nor do we guarantee their accuracy or completeness.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Capital Wealth Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or Capital Wealth Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!