- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 18, 2022 at 11:15 am

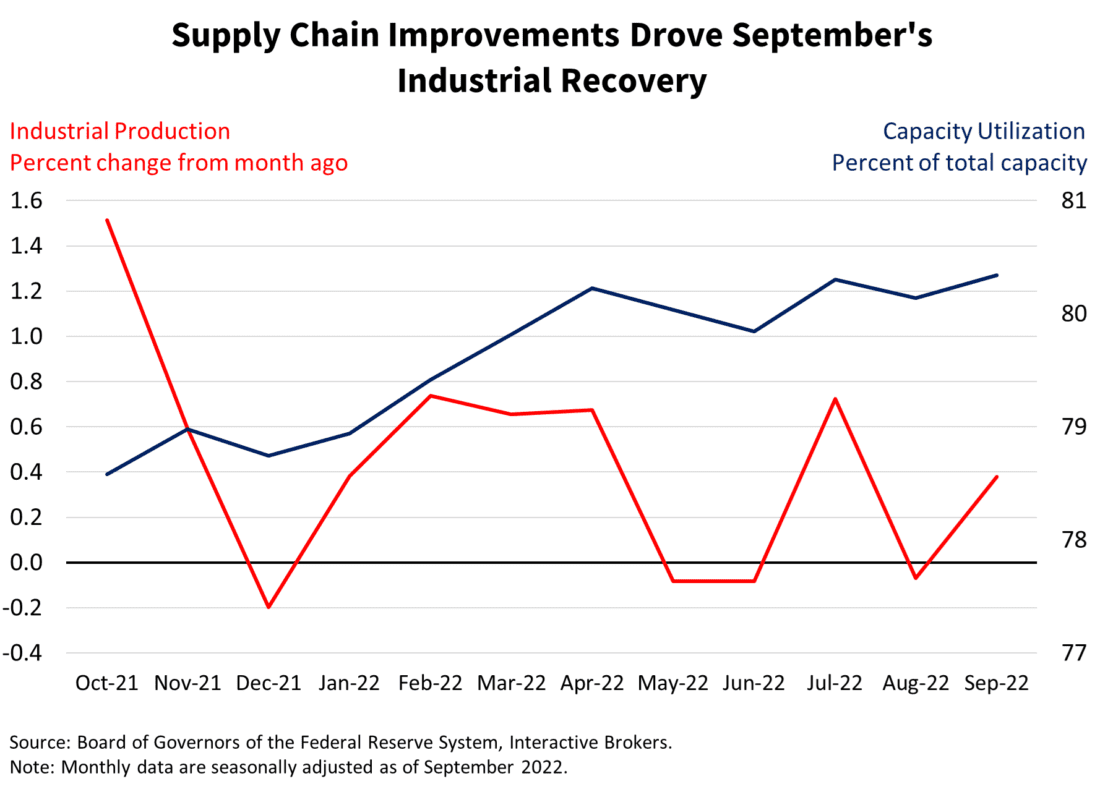

Industrial production and capacity utilization data released today appear favorable for GDP while providing somewhat mixed messages about inflation. Industrial production notched a 0.4% month-over-month gain, better than expectations of 0.1% and a recovery from August’s 0.1% decline. On a year-over-year basis, September’s gain came in at 5.3%, better than August’s 3.9% reading. Capacity utilization recovered back to the July level of 80.3 after falling to 80.1 in August. Gains were broad based across major market and industry groups and driven largely by supply chain improvements.

On an optimistic note, higher industrial production and capacity utilization are positive on the inflationary front because more goods being produced offers more supply for consumers to bid on, softening price pressures as consumers have more options.

At the same time, capacity utilization, or the percentage of the industrial sector’s production capabilities being used, implies that efficiencies are improving, a deflationary development. Within today’s data release, furthermore, business equipment had the largest year-over-year production increase, reaching 8.2%, implying that the economy’s production capacity is increasing and that business sentiment about the economy may be improving.

Industrial activity, however, is expected to slow in the coming months due to the shift in spending from goods to services, tightening financial conditions, slower economic growth and international challenges.

On balance, today’s report is favorable for GDP. Increasing production and higher capacity utilization means that the demand for goods is rising and that production is improving. GDP is driven mainly by consumer spending in the U.S. and in most developed nations, so improving demand is encouraging.

The production of major market groups experienced strong recoveries that erased most of August’s losses. Construction, consumer goods and business equipment posted solid gains of 1.1%, 0.6%, and 0.5%, offsetting all of August’s weakness and adding gains on top. Materials also contributed to gains albeit more modestly. Major industries also performed well during the month with mining and manufacturing posting gains of 0.6% and 0.4%. Utilities offset some of the progress with a contraction of 0.3% during the period.

Watch the Industrial Production Educational Video at Traders’ Academy – Click Here

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!