- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 7, 2023 at 10:20 am

The disinflation process has begun.

Lower bond yields will likely follow.

Rate-sensitive, early-cycle stocks may benefit.

Are rising or falling bond yields good or bad for cyclical sectors? The answer is yes! While that may not seem like a serious response, it truly depends on the economy-sensitive sector in question at a given stage of the market cycle. As my regular readers know, I think we’re on the leading edge of a stock market recovery — it seems inflation has stabilized, the Federal Reserve may soon wind down interest rate hikes, but I believe the recovery will require the participation of the consumer discretionary sector. So let’s start there.

As an equity strategist, I care about the direction of interest rates — especially the 10-year US Treasury bond yield — because they’re the discount rate for stocks. As we saw through much of 2022, rapid increases in bond yields can dramatically lower the present value of businesses’ expected cash flows. As we’ve seen since October of the same year, however, that process can also work in reverse (i.e., lower bond yields and higher share prices).

One way for investors to get their arms around the prevailing direction of interest rates is by assessing the outlook for the general level of prices in the economy.

Anyone on a fixed income over the past few years understands how accelerating prices for basic necessities — food, rent, medical care, energy, cars, etc. — sap their ability to spend on other more discretionary items. Contrastingly, decelerating prices boost consumers’ ability to spend on discretionary things.

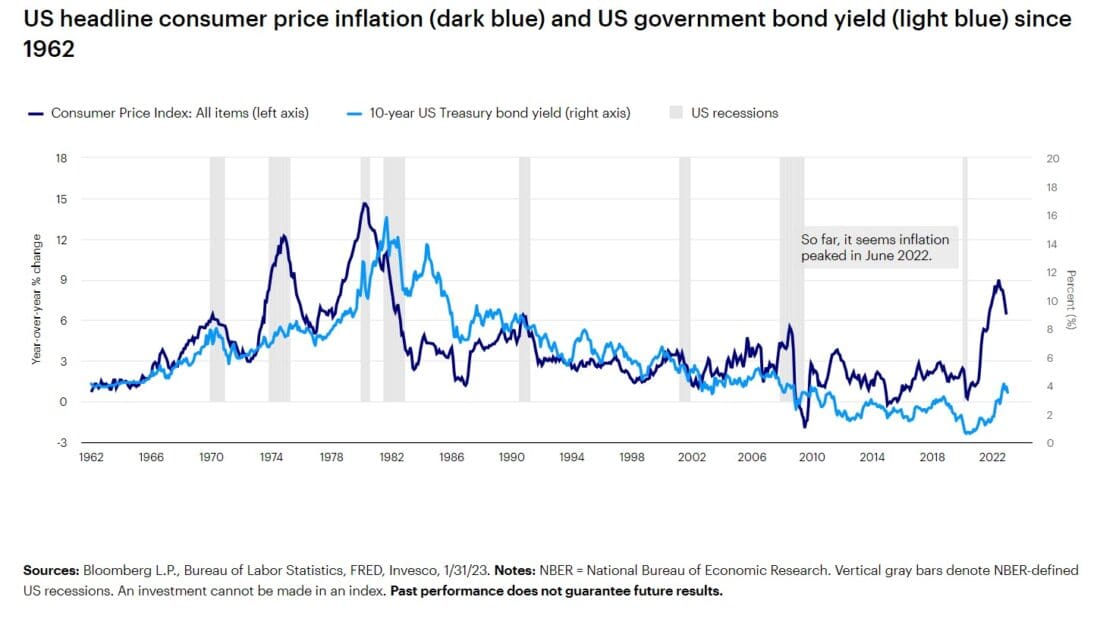

The same principle applies to the bond market. Faster inflation takes a real bite out of fixed coupon payments, thereby reducing the value or attractiveness of outstanding debt issues (Figure 1). Meanwhile, disinflation or outright deflation have the opposite effect (i.e., higher bond prices and lower bond yields).

In a February 7, 2023, speech, Federal Reserve (Fed) Chairman Jerome Powell said, “The disinflationary process, the process of getting inflation down, has begun…,”1 an official statement that ratifies my favorable views on the general level of prices and bond yields.

In fact, the symmetrical roundtrip of the Institute for Supply Management (ISM) Manufacturing Prices Index — from its trough of 35.3 in April 2020 to its peak of 92.1 in June 2021 and back to contraction territory since September 20222 — suggests a strong whiff of outright deflation in the goods sector.

Powell added that in the non-housing sector, “Services [are] not really showing any disinflation yet.”1 From my lens, however, the annualized 3-month percent change in the Consumer Price Index (CPI) for services excluding shelter has plummeted to a low single-digit pace. Perhaps the “immaculate” disinflation scenario I first wrote about in May 2022 is playing out.

Powell also mentioned that taming inflation “will be a process that takes a significant period of time.” However, I suspect policymakers and investors will be caught off guard by how quickly the disinflationary impulse asserts itself. On a year-over-year basis, headline CPI decelerated for the seventh consecutive month in January 2022, an observation that seems to have escaped recent market commentary.

In a finance-based economy dominated by consumers, the relationship between interest rates and spending is intuitive. When the cost of money or debt rises, consumers think twice about applying for mortgages to buy a house, loans to buy cars, and credit cards to finance spending on other goods and services.

When interest rates fall, however, debt-fueled consumption becomes more manageable, thereby improving households’ financial outlook.

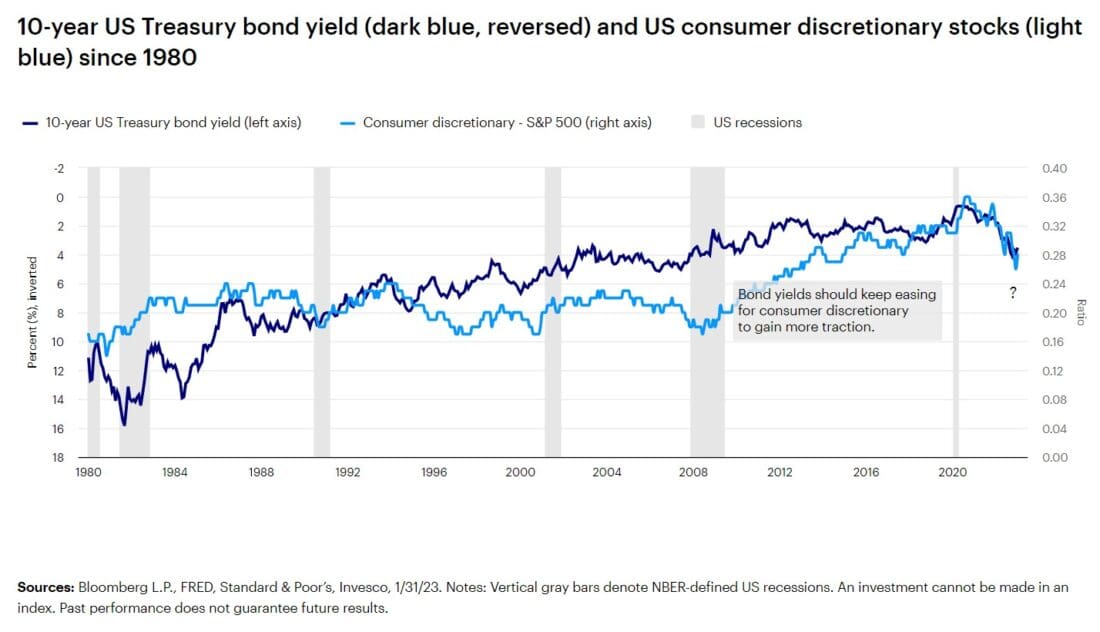

If I’m right about an inflection point in consumer prices, declining bond yields, and a calmer Fed reaction function, those dynamics should support rate-sensitive, early-cycle consumer discretionary stocks (Figure 2).

After a period of normalization and recovery, I’d expect inflation and bond yields to eventually drift higher once again on the back of an expanding economy.

If what’s past is prologue, that stage of the market cycle and change in the direction of interest rates will likely have a different effect on other later-cycle sectors such as financials, industrials, and materials. But that’s a story for another day.

Footnotes

—

Originally Posted March 3, 2023

How do bond yields affect cyclical sectors in the stock market? by Invesco US

Important information

NA2764075

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

All investing involves risk, including the risk of loss.

Diversification does not guarantee a profit or eliminate the risk of loss.

Past performance does not guarantee future results.

Investments cannot be made directly in an index.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

A bond’s yield is the return to an investor from the bond’s interest, or coupon, payments.

A cyclical sector is an equity sector whose price is affected by ups and downs in the overall economy.

The discount rate refers to the rate of interest that is applied to future cash flows of an investment to calculate its present value. It is the rate of return that companies or investors expect on their investment.

Inflation is the rate at which the general price level for goods and services is increasing.

Disinflation, a slowing in the rate of price inflation, describes instances when the inflation rate has reduced marginally over the short term.

Deflation is a decrease in the general price level of goods and services that occurs when the inflation rate falls below 0%.

The Consumer Price Index (CPI) measures change in consumer prices as determined by the US Bureau of Labor Statistics. Core CPI excludes food and energy prices while headline CPI includes them.

Aninflection point isan event that results in a significant positive or negative change in the progress of a company, industry, sector, economy or geopolitical situation.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of manufacturing firms in the US, monitors employment, production, inventories, new orders and supplier deliveries.

The S&P 500® Index is a market-capitalization-weighted index of the 500 largest domestic US stocks.

The opinions referenced above are those of the author as of March 3, 2023. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!