- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 12, 2024 at 10:45 am

Markets are bouncing back from yesterday’s risk-off sentiment despite this morning’s releases of a hotter-than-anticipated PPI and weaker-than-projected Consumer Sentiment data. Investors are indeed piling into everything, as short- and long-term inflation expectations ticked down in today’s UMich print, sending odds of a September rate reduction from the Fed upward to 90%. A critical risk, however, lies in financial conditions loosening, a development that is already contributing to our real-time tracking measures pointing to July inflation of 0.3% m/m for headline and core. A continuation of these developments, which is my base case, will deter the Fed from dishing out its first cut of the cycle in September, opting for December instead.

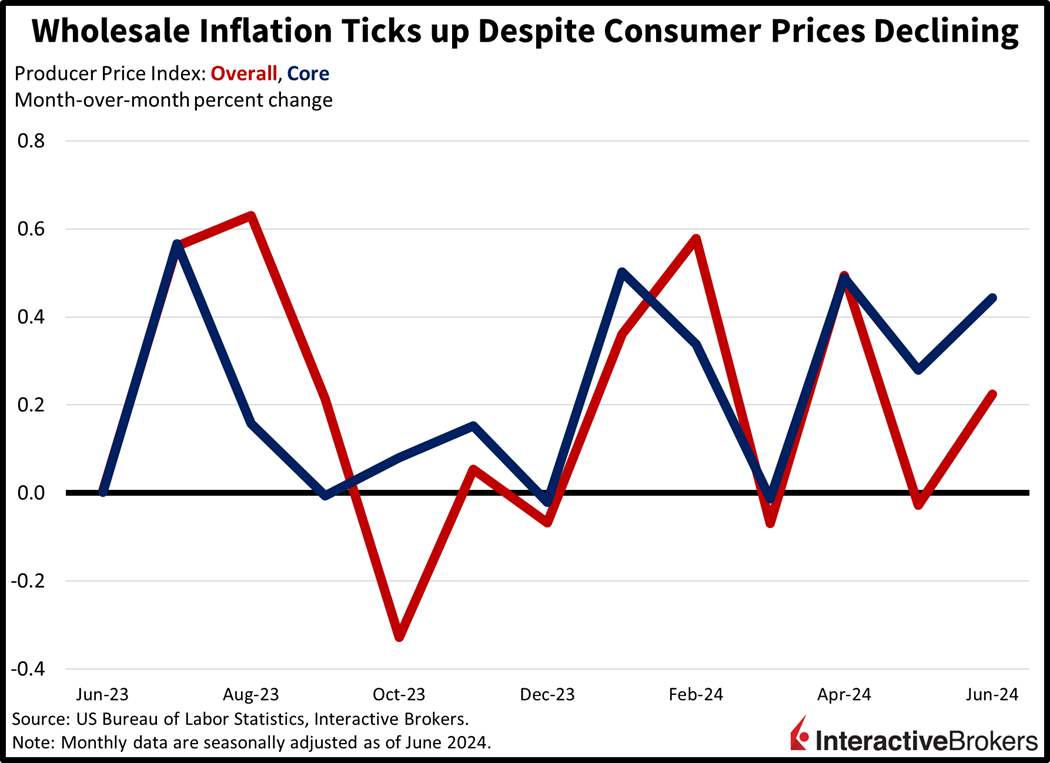

June wholesale prices rose despite deflation in energy, food and in the transportation and warehousing category. The Producer Price Index (PPI) rose 0.2% month over month (m/m) and 2.6% year over year (y/y), stronger than the 0.1% and 2.3% projected as well as the -0.2% and 2.2% in May. Similarly, core figures, which exclude food and energy, posted upside beats of 0.4% m/m and 3% y/y, loftier than the median estimates of 0.2% and 2.5% and the previous month’s 0.3% and 2.3%. While energy, the transportation and warehousing component and food saw charges drop 2.6%, 0.4% and 0.3%, trade services and other services experienced cost increases of 1.9% and 0.1%.

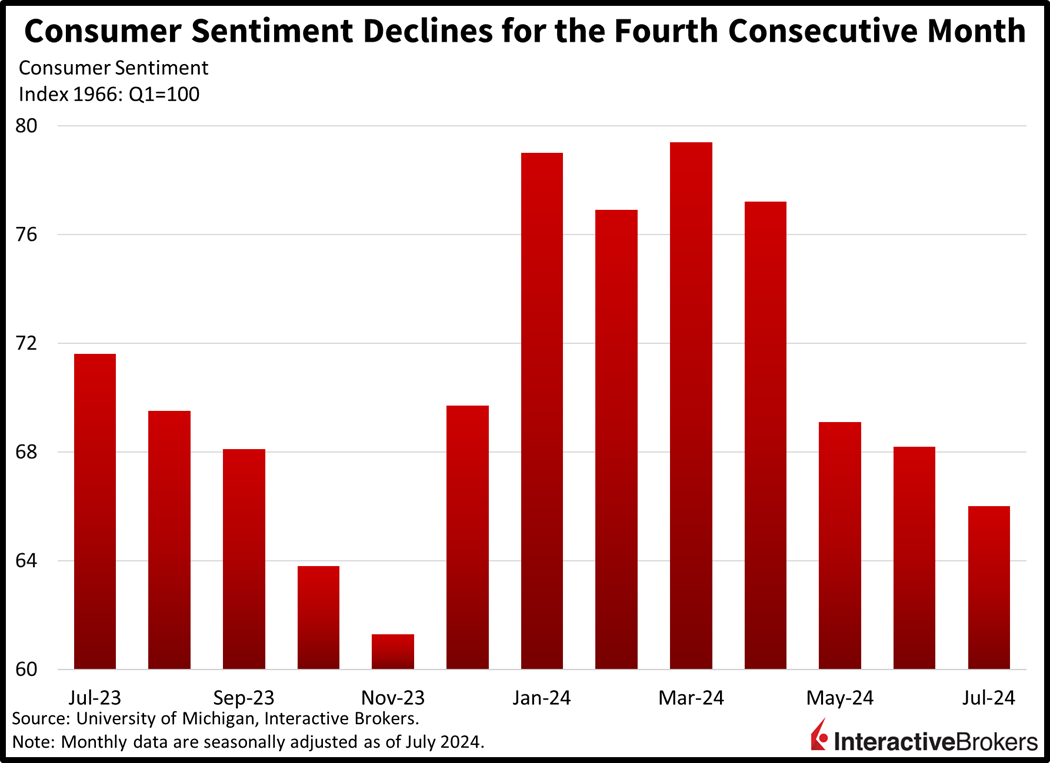

Folks are currently feeling the lousiest they have this year regarding the economy and their finances, with the University of Michigan’s (UMich) Consumer Sentiment Index declining for the fourth consecutive month. Sentiment dropped to 66, beneath projections of 68.8 and June’s 68.2. Both sub-indices for current conditions and future expectations sunk to 64.1 and 67.2 from 65.9 and 69.6 during the period. Meanwhile, inflation expectations for one- and five-year periods both dropped from 3% to 2.9%. Still, consumers blamed elevated prices for their sour moods, while uncertainty concerning November’s presidential election also weighed upon sentiment.

Corporate CFOs continue to emerge from their capital raising hibernation, helping JPMorgan Chase, Citigroup and Wells Fargo beat analyst consensus expectations for second-quarter earnings and revenue. The increased capital raising activity follows a pickup in investment banking earlier this year that helped Morgan Stanley and Goldman Sachs post strong first-quarter results. Today’s better-than-anticipated earnings releases, however, featured commentary regarding potentially persistent inflation and high interest rates. Credit losses also emerged. Consider the following earnings highlights:

Asset prices are rewarding market bulls with stocks and bonds levitating alongside some of the cyclical commodities. All major US equity indices are gaining, with the Russell 2000, Nasdaq Composite, S&P 500 and Dow Jones Industrial benchmarks higher by 1.5%, 1.1%, 0.9% and 0.8%. Sectoral participation is terrific—every segment is higher. Piloting the bulls are consumer discretionary, technology and industrials, which are flying north by 1.6%, 1.4% and 1%. Treasurys are catching bids as well with the 2- and 10-year maturities changing hands at 4.48% and 4.20%, 4 and 2 basis points (bps) lighter on the session. Softer borrowing costs, heightening Fed easing wagers and decelerating economic prospects are weighing on the dollar, with its index down 39 bps. The greenback is losing ground relative to each of its major counterparts minus the yuan. It’s down versus the euro, pound sterling, franc, yen and Aussie and Canadian dollars. Commodities are mixed with copper and crude oil higher by 1.3% and 0.4% but lumber, silver and gold lower by 2.4%, 1.8% and 0.2%. WTI crude is trading at $83.28 per barrel on a lighter supply outlook amidst stable demand prospects.

While yesterday’s market trading demonstrated enthusiasm for small caps and value, the economy has created an increasingly narrow path for those categories to outperform, a development that is likely to put even more significance on the ability of the Magnificent Seven to power market gains. I see two possible scenarios going forward. One scenario is the much hoped for soft landing, which is likely to feature elevated interest rates and investors requiring a significant risk premium as a result. These factors would create a strong headwind for rate-sensitive small-cap companies and value-tilted sectors that lack exciting narratives to drive multiple expansion. The second possible scenario—recession—would create revenue challenges for all corporates, but it would be particularly painful for small-cap firms which carry slim margins in aggregate. In this environment, value names are also likely to struggle because, their only answer to revenue pressures would be to reduce expenses, generally speaking. In either scenario, it will be essential for the Magnificent Seven to continue to generate revenue and earnings growth by disrupting existing industries with new products, such as artificial intelligence, robotaxis’, automation and ledgers associated with blockchain technology. But given the recent runup amidst eye-watering valuations and an equity risk premium that is negative when compared to short-term yields and in the basement relative to the long-end, the risk of a significant drawdown in the 20% range is certainly in the cards.

Visit Traders’ Academy to Learn More About the Producer Price Index and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

Need to pass out more “free money.”