- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 28, 2023 at 12:11 pm

With investors still assessing the impact of inflation’s U.S. resurgence, new data shows that price increases are also rebounding in France and Spain. U.S. home price data released today, however, show that the sector is far from recovering, especially as we navigate this new “higher for longer” regime. Home prices have declined for six consecutive months with no relief in sight. Amidst the sea of discouraging news, U.S. consumer confidence data released this morning was ice cold, favorable for fighting inflation, but at a significant implied cost—declining consumer spending which represents approximately 70% of the country’s GDP. As the U.S. Federal Reserve’s monetary tightening continues to raise fears that the country is likely to slip into a recession, Canada’s recent GDP release of 0%, shows the Great White North may be heading for an economic freeze.

U.S. home price data released today, however, show that the sector is far from recovering, especially as we navigate this new “higher for longer” regime. Home prices have declined for six consecutive months with no relief in sight.

Markets are looking to enter the new month directionless for the most part. The S&P 500 index is virtually unchanged, with gains from tech offsetting some weakness in the industrials. The Nasdaq is up 0.2% while the Dow is down 0.3%. Yields bounced notably earlier this morning in response to hot Euro inflation data but cool U.S. consumer confidence subdued yields back to unchanged levels. Adding to the snooze fest is the dollar index, skipping from gains to losses and then settling at an unchanged level. Crude oil is moving strongly this morning, however, as incoming economic data from China is expected to show a strong economic recovery. Chinese momentum offset concerns of a U.S. economic slowdown, as traders drove prices 2.4% higher to $77.50 per barrel.

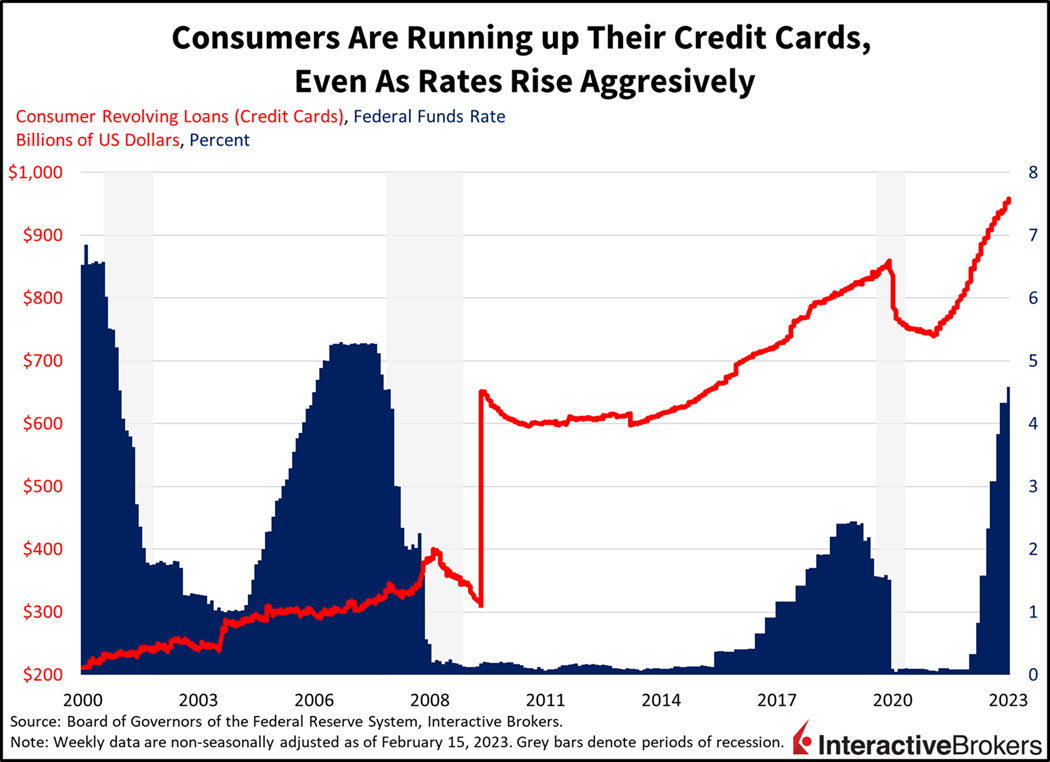

Recent data include the following:

With growing fears about a resurgence in inflation, investors face a challenging start to March. Upcoming job market data on Friday, March 10th and results for the next Consumer Price Index are like to be too strong for the Fed and market sentiment may hinge, in part, on the potential for tight labor conditions to fuel wage pressures and the ability of consumers to continue spending as they burn through COVID-19 stimulus payments and increasingly use credit cards to finance their expenditures. How consumers manage their rising variable rate debt burdens, the delayed effect of Fed rate hikes, the impact of future rate increases and persistent inflationary pressures will determine the path of economic performance and asset valuations in 2023.

Visit Traders’ Academy to Learn More about Consumer Confidence, Home Prices, Gross Domestic Product and Other Economic Indicators.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!