- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 14, 2023 at 12:15 pm

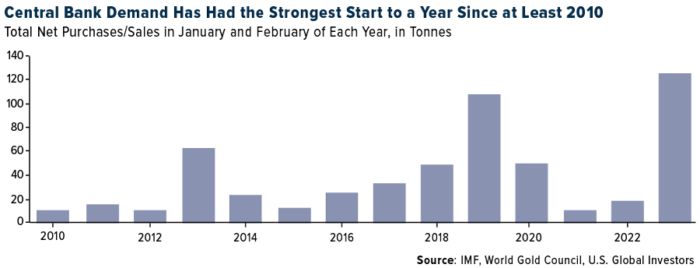

Central banks accumulated gold at the fastest pace on record in the first two months of 2023, according to a report by the World Gold Council’s (WGC) Krishan Gopaul. In January and February, central banks collectively bought a net 125 tonnes of the metal, the highest amount for the year-to-date period since banks became net buyers in 2010.

The countries reporting the largest purchases in the first two months were Singapore (51.4 tonnes), Turkey (45.5 tonnes), China (39.8 tonnes), Russia (31.1 tonnes) and India (2.8 tonnes). The Central Bank of Russia published an update on its gold reserves for the first time in about a year, so the 31.1 tonnes were likely accumulated over the course of several months instead of in January and February.

Meanwhile, very few countries’ central banks shrank their gold reserves. Net sellers were Kazakhstan, Uzbekistan, Croatia and the United Arab Emirates (UAE), though year-to-date purchases far outweighed sales.

If you look back at the list of net buyers, you’ll notice that three are members of the BRICS countries (Brazil, Russia, India, China and South Africa). I point this out because, as I’ve been sharing with you for a couple of weeks now, we may be seeing the emergence of a multipolar world, with a U.S.-centric world on one side and a China-centric world on the other. For the first time ever, BRICS countries’ share of the global economy has surpassed that of the G7 nations (Canada, France, Germany, Italy, Japan, the U.K. and U.S.), on a purchasing parity basis.

Gold plays an important role in this multi-polarization. The BRICS need the precious metal to support their currencies and shift away from the U.S. dollar, which has served as the global foreign reserve currency for about a century. More and more global trade is now being conducted in the Chinese yuan, and there are reports that the BRICS—which could eventually include other important emerging economies such as Saudi Arabia, Iran and more—are developing their own medium for payments.

If this is indeed the case, the implication is clear to me that investors should be increasing their exposure to gold and gold miners. Gold is a finite resource. It’s expensive and time-consuming to produce more of it. At the same time, BRICS countries will continue to be net buyers as they seek to diversify away from the dollar.

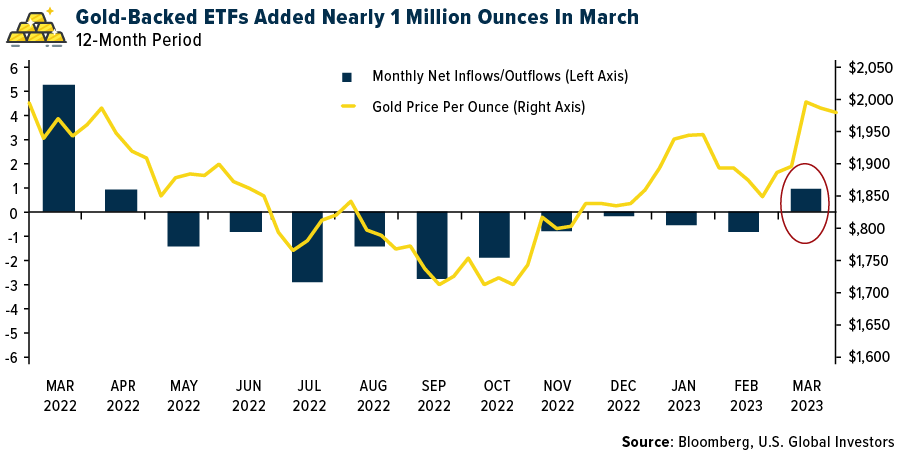

Net inflows into gold-backed ETFs turned positive in March after 10 straight months of outflows as the metal’s price flirts with a new record high. Investors added nearly 1 million ounces to all known physical gold ETFs in March, the highest monthly increase since March 2022, when investors added 1.4 million ounces. As of March 31, total gold holdings stood at 93.2 million ounces, according to Bloomberg.

In light of weak economic news, ongoing inflation, rising rates, a shaky banking sector and geopolitical tension, gold is catching a strong bid as it seeks to make a new all-time high. On Thursday, the metal touched $2,032 an ounce, just $43 off its record high, set in August 2020.

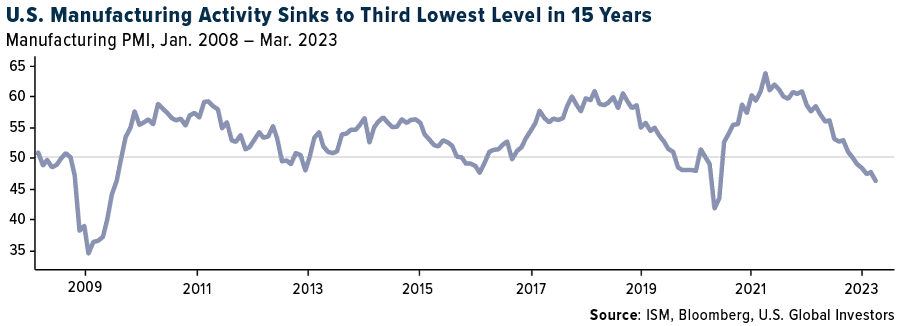

I believe accumulating gold and gold stocks is prudent and wise at this time, especially as recession signals are starting to flash. U.S. manufacturing activity contracted at a faster rate for the fourth straight month, with ISM’s Manufacturing PMI sinking to 46.3 in March. That’s the third-lowest reading in 15 years, following the financial crisis and pandemic lockdowns. What’s more, every category—from new orders to production to inventories—was in contraction mode.

The Federal Reserve’s actions to slow economic growth appear to be having the desired effect. We may be looking at the end of the most aggressive rate hike cycle in two generations, and this carries risks that investors should be aware of.

Over the past 70 years, a Fed pause was followed by an economic recession 75% of the time, with an average lag of six months, according to CLSA’s Alexander Redman and Della Chen. The two analysts believe the Fed has just one more hike to go before it pauses and begins to reverse course. The cycle should be complete by July, Redman and Chen estimate.

If their estimates are correct, we may be looking at a recession late in the fourth quarter.

The time to buy equities, they say, is when the Manufacturing PMI bottoms after the start of the recession. Doing so resulted in positive 12-month returns seven out of eight times, for an average return of 26%.

Timing these things is always tricky, and we’re talking about events that could be months in the future. If a recession is in the cards, it may make sense to ride it out with the help of gold. As always, I recommend a 10% weighting, with 5% in physical gold and the other 5% in high-quality gold mining stocks, mutual funds and ETFs.

—

Originally Posted April 10, 2023 – Central Banks’ Gold-Buying Spree: Implications For The Global Economy And Investors

The ISM Manufacturing Index, commonly known as the ISM Manufacturing Purchasing Managers Index (ISM PMI), is a monthly gauge of the level of economic activity in the manufacturing sector in the United States versus the previous month.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!