- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 2, 2024 at 11:00 am

Markets are little changed as investors listen to Fed Chief Powell and his global counterparts discuss economic prospects and the path of monetary policy. On balance, central bankers seemed to air on the side of caution regarding the risks of a renewed uptick in price pressures. Meanwhile, the economic calendar featured hotter-than-expected core inflation and labor data from the EU and US, respectively.

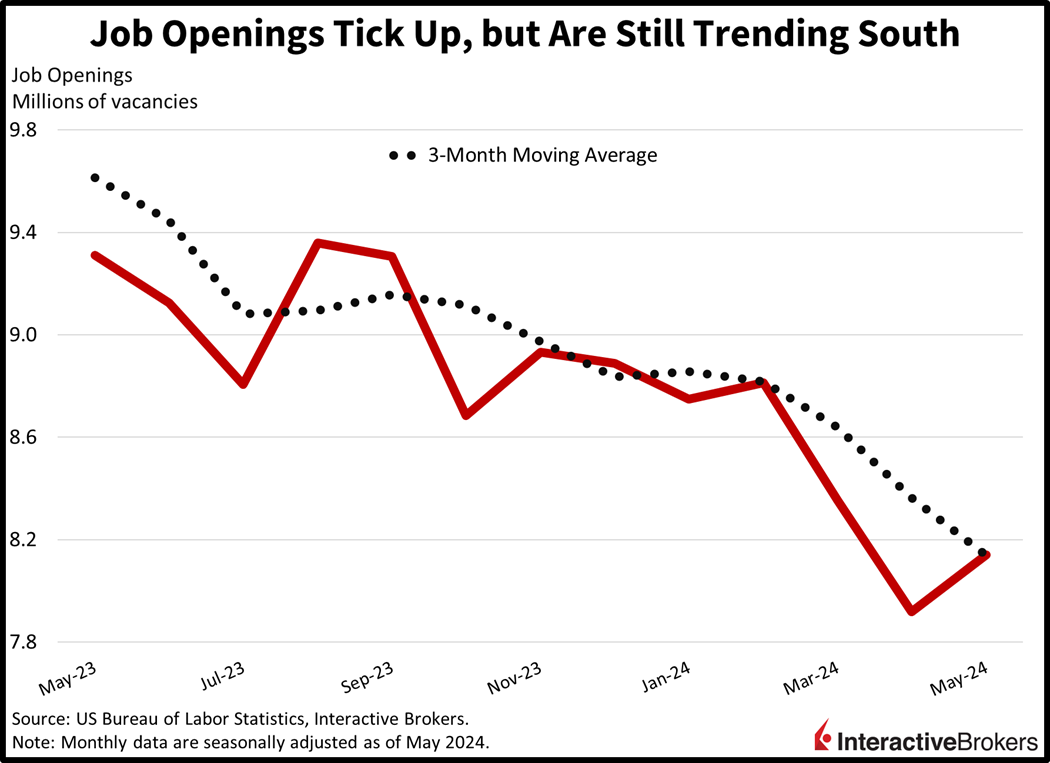

Labor demand picked up steam in May, according to this morning’s Job Openings and Labor Turnover Survey. Job openings posted a sizable upside beat of 8.14 million considering the consensus anticipated a decline to 7.91 million. In comparison, April arrived at 7.92 million. Job quits also increased, pointing to rising confidence among workers in their ability to find employment elsewhere. Quits rose from 3.452 million to 3.459 million during the period.

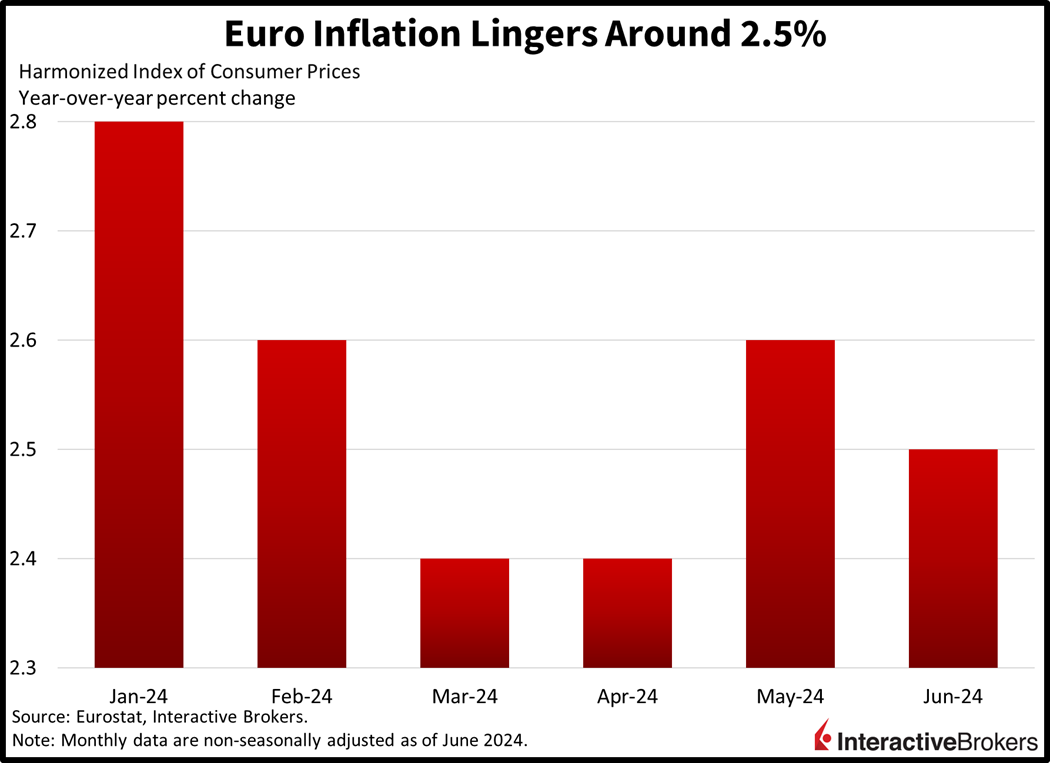

The euro area made further progress in subduing price pressures last month as goods and commodities offset stubbornness in the labor-intensive services sector. Headline prices rose 0.2% month over month (m/m) and 2.5% year over year (y/y), in-line with expectations and near May’s 0.2% and 2.6%. Core prices, however, increased 0.3% m/m and 2.9% y/y, above projections of 0.2% and 2.8% and near the previous month’s 0.4% and 2.9%. June inflation was driven by a 0.6% m/m rise in service charges and a 0.2% increase in costs for the processed food, alcohol and tobacco category. On the other hand, deflation was present in energy, unprocessed food and industrial goods with m/m prices declining 0.8%, 0.4% and 0.1% during the period.

Fed Chair Powell this morning told attendees at the European Central Bank Forum in Sintra, Portugal, that US disinflation has resumed, and he is encouraged by recent data pointing to easing price pressures. The Fed wants more proof that this trend is continuing before cutting rates. When asked when he envisions the central bank easing policy, Powell pushed back, saying he won’t provide an expected date for the change, but he added that an unexpected softening of the job market could prompt policymakers to dish out incremental accommodation sooner than expected. For now, the Fed can take its time with reducing borrowing costs because the labor market is still strong and the economy is growing. Conversely, demand for workers has eased slightly, helping to soften wage pressures that have contributed to cost increases. He also reiterated the Fed’s challenge of maintaining a restrictive stance to prevent a resurgence in price increases while ensuring that monetary policy is eased prior to the economy dipping into a recession.

Markets are uneventful today despite central bankers taking the stage and a slew of economic data hitting the tape. Major US equity indices are mixed. The Dow Jones Industrial and S&P 500 benchmarks are both down 0.1% while the Nasdaq Composite and Russell 2000 baskets are 0.2% and 0.1% higher. Sectoral breadth is split, with six out of eleven sectors pointing north on the session. The consumer discretionary, utilities and financials segments are leading the bulls with gains of 1.3%, 0.3% and 0.2%. Leading the charge to the downside are the healthcare, materials and technology components which are losing 0.5%, 0.3% and 0.2%. Treasury yields and the dollar are near the flatline, with the 2- and 10-year maturities changing hands at 4.72% and 4.44%. The greenback is gaining relative to the euro, franc, yen, yuan and Aussie dollar but is down versus the pound sterling and Canadian dollar. Commodities are mixed, with silver, copper and lumber up by 0.9%, 0.8% and 0.4% but gold and crude oil are close to unchanged.

With conference attendees this morning appearing to focus on a possible September rate cut, the next three months of inflation reports will be crucial for both investor sentiment and policymakers’ timing for turning dovish. It’s likely that June will show continued disinflation but the potential results for July and August are less clear, raising the question of how many months of favorable data are needed before the Fed makes the move. In the meantime, oil prices are a significant inflationary factor with the commodity’s price hitting a two-month high in response to growing geopolitical tensions, including Israel stepping up its military offensive against Hezbollah in Lebanon. While navigating a maze of economic data, the Fed is also cognizant of the upcoming November presidential election and the risk of appearing political if it shifts before voting begins, creating a deterrent for a September rate cut.

Visit Traders’ Academy to Learn More About Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!