- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 9, 2025 at 12:05 pm

The Federal Reserve meets tomorrow to decide whether to deliver another 25 bps rate cut, and that decision runs straight through its dual mandate: maximum employment and price stability. On paper, those goals seem aligned. In reality, they often pull in opposite directions – easing too much risks reigniting inflation, tightening too long risks weakening the labor market.

According to the IBKR Forecast Trader, 96% of participants expect a rate cut, so markets are clearly leaning toward more easing. How the Fed votes tomorrow will reveal how it’s weighing that tension right now, and how much risk it’s willing to take on either side of the mandate.

The employment side of the mandate is about keeping the labor market strong and inclusive. In plain terms, the Fed wants:

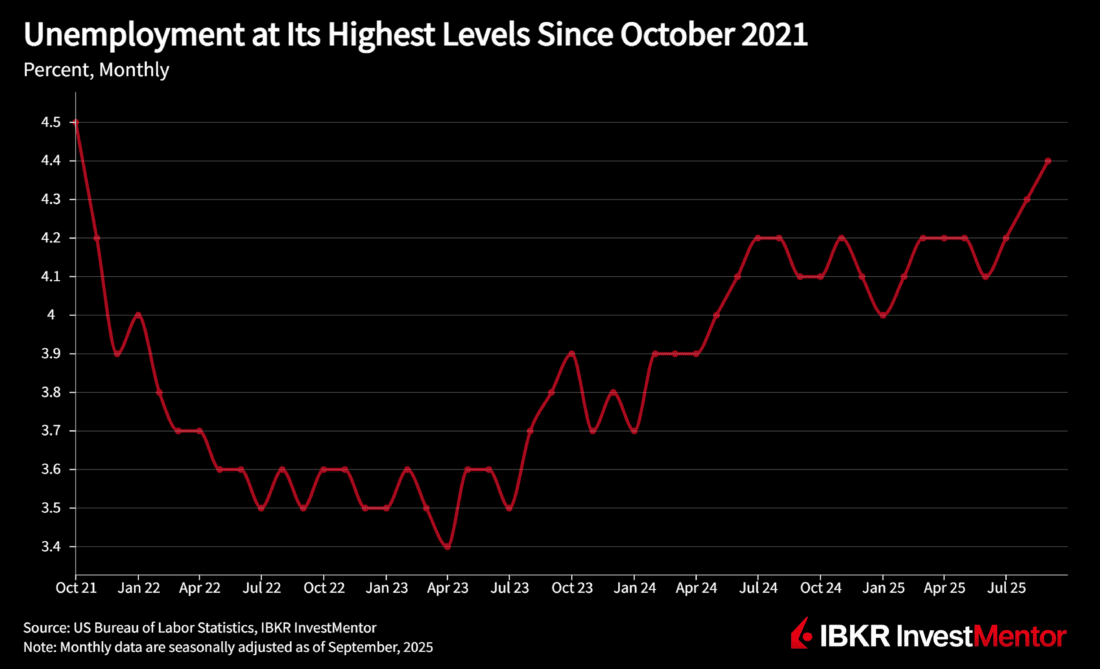

The challenge is that there is no fixed, universal number for “maximum employment.” It is not a specific unemployment rate. It depends on demographics, productivity, labor force participation, and the structure of the economy at a given time.

When the job market runs very hot, you see:

From a social and political standpoint, that is attractive. The Fed is usually reluctant to step on the brakes when the gains are finally reaching more workers, especially lower-income and historically marginalized groups.

But there is a risk: a labor market that runs too hot for too long can feed inflation pressure. Firms facing higher wage costs may try to pass those costs along via higher prices, especially in sectors where demand is still strong.

On the inflation side, the Fed aims to keep prices stable by holding PCE inflation at about 2% over time. In reality, inflation has stayed above that goal, with the latest data showing both headline and core PCE running at roughly 2.8% year-over-year.

Price stability is less visible than job gains, but just as important. It matters because:

Here the Fed’s key asset is credibility. If households and businesses believe the Fed will eventually bring inflation back to around 2%, their long-term expectations remain anchored. That, in turn, makes it easier to achieve the target without over-tightening.

The difficulty is that getting inflation down often requires tighter financial conditions: higher interest rates, weaker demand, slower hiring, and sometimes higher unemployment. In other words, success on the inflation side of the mandate can require trading off some near-term strength on the employment side.

The most challenging moments for the Fed are not when both sides line up (weak labor market and low inflation, or strong labor market and stable inflation), but when they diverge.

Typical late-cycle setup:

If the Fed focuses too heavily on employment, it risks letting inflation become entrenched, which would eventually require even more painful tightening to fix. If it focuses too heavily on inflation, it risks over-tightening and triggering a recession that pushes unemployment higher than necessary.

The dual mandate forces the Fed to weigh both risks:

Markets spend a lot of time guessing which side the Fed is prioritizing at any given moment.

Complicating all of this are lags. Monetary policy works with delays:

That means the Fed is always making decisions based on imperfect, backward-looking data:

On both sides of the mandate, the Fed is effectively setting policy for the economy it expects to see 6–18 months from now, not just the data it has in front of it.

For investors, understanding the dual mandate is less about memorizing the Fed’s 2% target and more about reading how the tradeoff is evolving:

When employment is healthy and inflation is close to target, the Fed has room to be patient.

When inflation is above target and the labor market is still tight, the Fed tends to lean harder toward price stability, even at the cost of some near-term job softness.

The dual mandate is not a neat optimization problem with a simple formula. It is an ongoing balancing act, where the Fed has to protect the long-run benefits of low, stable inflation while recognizing the real human costs of weaker labor markets.

For anyone following policy, the key is to watch both sides of the mandate together, not in isolation: how each new jobs report and inflation print shifts the Fed’s perception of that balance, and how that, in turn, shapes the path of interest rates, financial conditions, and ultimately asset prices.

To learn more about how monetary policy affects you, download IBKR InvestMentor.

Learn more about InvestMentor

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!