- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 29, 2023 at 9:43 am

This post deals with the generalized least squares (GLS) estimator. When deriving the Black-Litterman (BL) model, the Theil mixed estimator is used, which is a kind of GLS.

Generalized Least Squares (GLS)

Black-Litterman (BL) model is based on Theil mixed estimator which is a kind of the GLS estimator.

Since BL model combines two regressions (market + views) which have different variance terms respectively, the conbined BL regression model has two different variance terms naturally. Unlike OLS with a constant (homogenous) variance term, when variance terms are not constant (heterogeneous), it is natural to apply the GLS estimator to get estimated parameters.

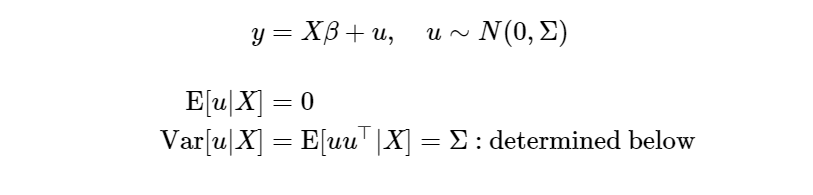

The starting point is a linear model.

As we are familar, OLS estimator has the following form with a constant variance term across all observations.

Hance, OLS estimator is of the following formula.

Our focus in on the GLS estimator for the linear regression model with non-constant variance terms (Σ = σ2Ω) across all observations, which means that residuals are heteroscedastic and/or serially dependent.

GLS estimator is of the following formula.

or

When Ω is symmetric, using eigen decomposition, Ω can be expressed as follows,

Here, A and Λ are eigenvector and eigenvalue matrix respectively.

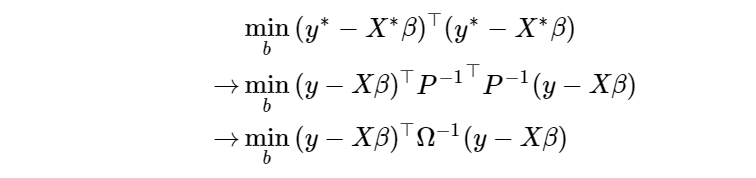

Now Ω can be transformed into the identity matrix (In) by multiplying P−1 in both sides

Multiplying P−1 on both sides of y = βX + u results in

Therefore, the linear regression model above is rewritten as

Least squares as the minimization problem is implemented as follows.

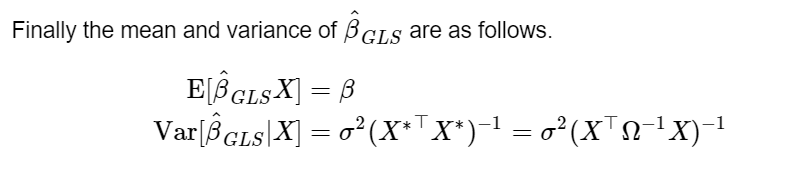

GLS estimator is

GLS estimator can be also expressed with the OLS estimator

This post derived the GLS estimator which will be used when deriving the Black-Litterman model.

Originally posted on SH Fintech Modeling blog.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SHLee AI Financial Model and is being posted with its permission. The views expressed in this material are solely those of the author and/or SHLee AI Financial Model and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!