- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 11, 2021 at 11:43 am

The article “ESG Performance Breakdown by E, S, and G” first appeared on Alpha Architect Blog.

The relationship among ESG ratings from third-party providers has historically produced conflicting results. Differences in sourced information and weighting schemes have produced low correlations between ratings and as a result, have handicapped the efforts to understand the relationship between ESG ratings and performance. Consequently, the credibility and willingness to use and invest utilizing ESG scores have been undermined for many investors. The authors of this article develop a “pillar” score approach that provides insight into three key economic channels related to ESG pillars, their components, and how they are combined. The analysis is then applied to the MSCI ESG rating methodology. The risk/return levels of individual E, S, and G pillar scores as well as the key issues related to the pillar scores are investigated. If you are so inclined to dig a bit deeper the authors have access to a video and a blog on the paper here.

The contribution of this work lies in the documentation of the relative significance of the issues that underlie a combined ESG rating. Although the study is confined to the MSCI ESG rating process, it provides much-needed insight into the theory of how the ESG “factor” is captured. Practically speaking, the analysis provides fodder for integrating ESG factors, pillars, and key issues into stock selection and/or portfolio construction. Of course, ESG investing necessarily imposes constraints on the investment opportunity set. All else equal, ESG investors should not expect to earn excess returns and must consider what factor exposures may lie beneath the surface. In short, always investors should ensure they understand what they own and why. This paper contributes to this discussion.

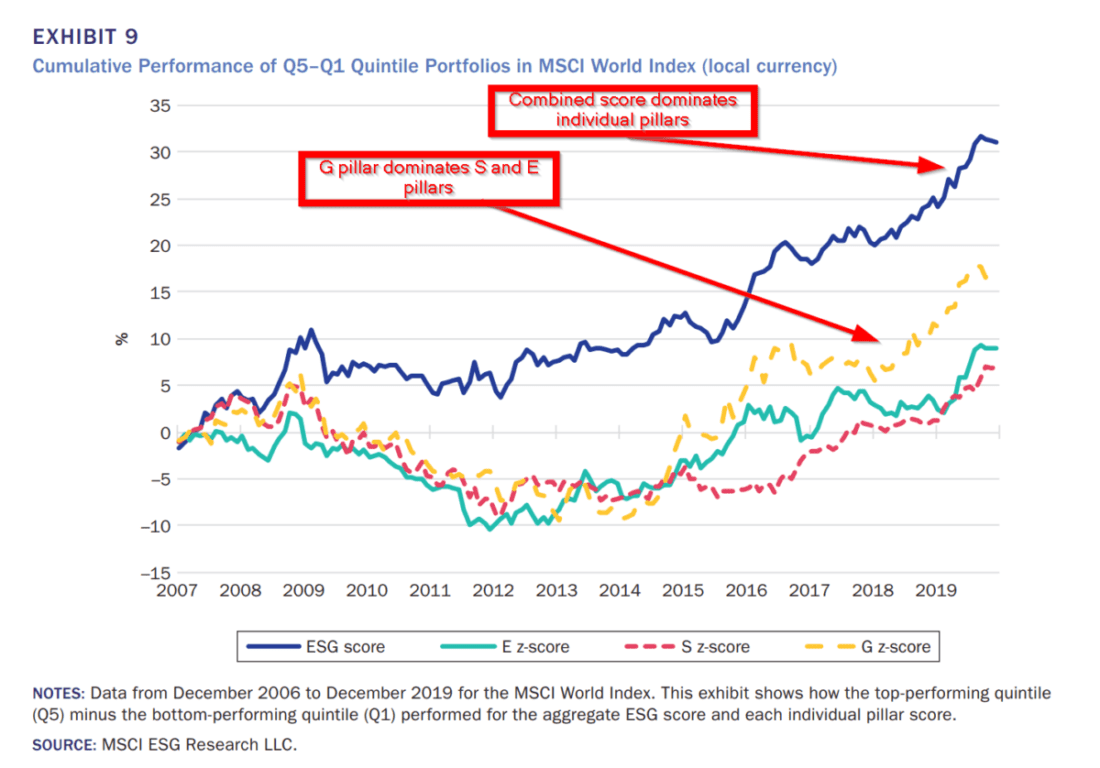

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

There are many ways to construct a company’s environmental, social, and governance (ESG) score or rating, involving different combinations of financial and nonfinancial inputs. Determining the most influential criteria for firm performance may be overlooked in the rush to “do some ESG.” In this study, the authors deconstruct ESG ratings performance at the E, S, and G pillar levels and use the most common key issues indicators that underlie ESG

scores. They find that the time horizon used has an important bearing on the indicators’ significance. In the short term, they find that governance is the dominant pillar because it strongly reflects event risks, such as fraud. In the long term, however, environmental and social indicators became more important because issues such as carbon emissions tended to be more cumulative, presenting erosion risks to long-term performance. The authors also find that a more balanced and industry-specific weighting of E, S, and G issues showed better long-term relevance than the individual pillar indicators alone.

Notes:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!