- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 15, 2021 at 1:47 pm

To be fair, what we’re about to discuss is not all that weird. I simply thought that if a headline like that works for clickbait generators, it might get more attention than “Compare VOLQ to VXN to Quickly Isolate the Implied Volatility of At-Money Options Versus Wings”. Admit it, the current headline is catchier, but the topic should be of interest to serious traders nonetheless.

Both VOLQ (NASDAQ-100 Volatility Index) and VXN (CBOE NDX Volatility Index)[i] measure the implied volatility of the NASDAQ 100 Index (NDX). Yet the methodologies have a crucial difference, and understanding that difference can offer market insight to traders.

The actual calculations are fairly complex, so I’ll leave it to mathematically curious readers to consult the exchanges’ websites for the methodologies (VOLQ here, VXN here). Both indices attempt to measure a constant 30 day implied volatility for NDX using a blend of options on strikes with an average time to expiration of 30 days (some shorter, some longer). Yet VOLQ uses a much smaller strike set of 32 near-money options, while VXN uses all strikes with non-zero bids.[ii] That means that VXN contains “wings” – out of the money options – while VOLQ does not. It also means that if we compare the two indices, we can get a quick approximation of the level of speculative and/or hedging activity in NDX.

I differ with NASDAQ about the value of out-of-the-money options. The VOLQ fact sheet states:

“Options which are out-of-the-money, particularly those which are extremely out-of-the-money, provide little insight to traders and investors yet they have outsized influence in traditional volatility indexes.”

My opinion is that out-of-the-money options (aka “wings”) do provide insight to investors. Below-market puts have been used as a portfolio hedging tool for decades. We recently noted the relatively high levels of put activity in our discussion of “fully invested bears.” Also, out-of-the-money put and call options have been used by speculators, with out-of-the-money calls taking on a new importance as a horde of new investors have entered the marketplace. Many newly-minted traders realized that options can have a similar payoff structure to sports bets (spend a fixed amount of money in the hope of making a leveraged return), and the relentless bull market over the past 18 months has offered ample opportunity for profitable speculation in call options – with the meme stock craze offering an extreme example.

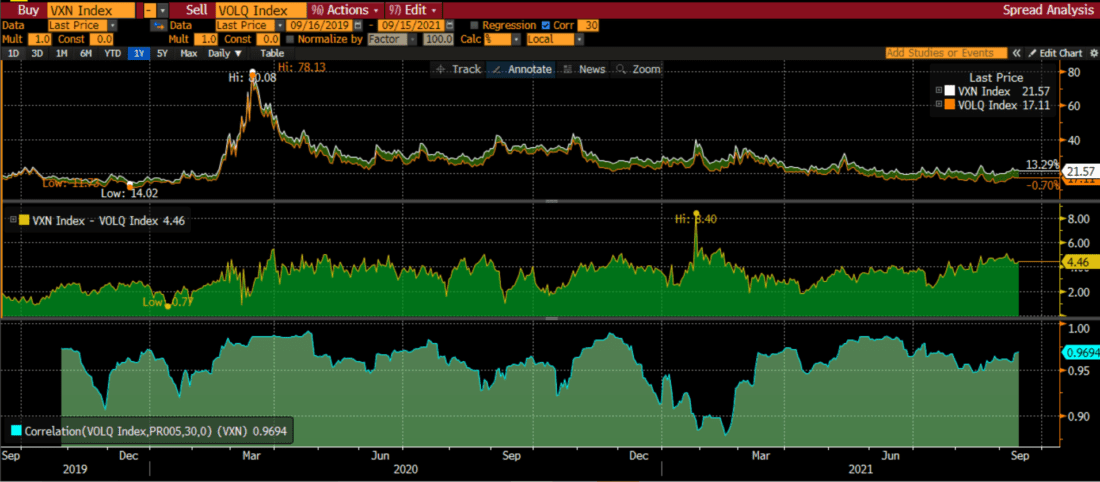

Out-of-the-money options typically trade with higher implied volatilities than their at-money counterparts. This phenomenon is called “skew”, and I urge you to read one of our previous pieces explaining skew if you don’t already understand the concept. It means that VXN should show a higher price than VOLQ because the former incorporates higher priced wings. The difference between the two should reveal the relative importance of wings versus at-money options at any given moment. The following graph illustrates that while the spread can change over time, the two indices remain highly correlated:

Source: Bloomberg

Interestingly, the peak spread between the two indices was on January 27th, during the height of the meme craze. Traders who were caught offside raced to purchase calls of any type in an attempt to hedge their exploding meme stock calls. We now see that VXN is trading at a relatively elevated level relative to VOLQ, though we are off the recent peak.

Unfortunately, this is an imperfect measure, because it fails to tell us exactly why the relative volatility of out-of-the-money options changed vis-à-vis their at-money counterparts. For that, we should consult a more detailed view of the options skew in NDX, as shown below:

Source: Bloomberg

We see that the implied volatilities of at- and below-market options rose while those of above-market options fell. The rise in at-money options boosted VOLQ and VXN alike, while the changes in the wings largely offset each other.

In short, I believe that NASDAQ has given us a new tool in VOLQ that we can utilize for volatility analysis. It can be used on its own, or in conjunction with VXN to determine the effect of wings on the relative pricing of options. The spread is useful – “a weird volatility trick”, as it were — but should be used as a first step for investigating whether puts or calls are driving the trading. As always, volatility is a nuanced topic, but one that can reward curious traders who understand those nuances.

—

[i] You should notice an oxymoron in the title of VXN. It is the CBOE’s measure of volatility on the most highly traded index of NASDAQ stocks. For obvious reasons it behooved NASDAQ to come up with a measure of their own, rather than utilizing a competitor’s calculations.

[ii] Again, I’m somewhat oversimplifying the methodology for the sake of brevity. Please consult the links if you want to get the exact details.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!