The presence of the January FOMC meeting on Tuesday and Wednesday puts most of the economic data in the shade. After the chilly tone to the FOMC statement and forecasts out of the December 17-18 meeting, expectations for a rate cut this week are practically nonexistent. When the meeting statement is released at 14:00 ET on Wednesday, it is unlikely to introduce any warmth. Fed Chair Jerome Powell’s press briefing at 14:30 ET on Wednesday will reflect the renewed caution about inflation and uncertainties about the economic outlook and conditions in the labor market.

In the absence of an interest rate move and with no update to the quarterly summary of economic projections (SEP), what can the statement and Powell’s question and answer period have to tell?

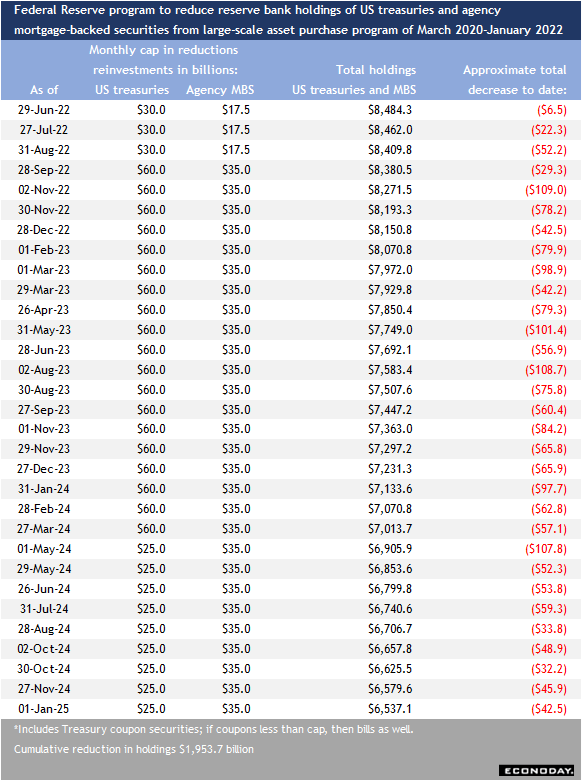

Primarily, there may be the initial communications regarding balance sheet policy. The Fed’s holdings of US treasuries and agency mortgage-backed securities is down nearly $2 trillion since June 2022 when the program to reduce the massive purchases of securities done during the pandemic crisis. On January 1, 2020 the total for US treasuries and agency mortgage-backed securities was about $3.74 trillion. To provide stimulus during the economic disruptions associated with the pandemic and because the fed funds target rate range was near the effective lower bound, the FOMC began another program of large-scale asset purchases – so-called quantitative easing or QE. The purchases peaked with holdings at $8.45 trillion in the August 3, 2022 week.

Powell has previously spoken about returning holdings of reserve assets from “abundant” to “ample” over time. The current balance of around $6.62 trillion is significantly higher than the June 2022 starting point. Nonetheless, the balance was never going to be as slow as it was in the pre-pandemic period since holdings tend to drift higher over time to meet technical requirements beyond monetary policy concerns. The balance is going to come down a bit more since any change to the program will probably be set for at least a couple of months from now. The start of the second quarter 2025 is a reasonable guess. An end to the program is a possibility since the cap on reinvestments of treasuries is $25.0 billion and the $35.0 billion cap for mortgage-backed securities is rarely, if ever, met. Whether an end or a reduction in caps, the Fed’s reserve bank holdings will continue to fall, but more slowly over a longer period.

On a side note, now that President Trump is in office, Powell is likely to receive a number of questions on fiscal policy and the independence of the central bank and its policymakers. Powell will reiterate and reinforce a message that he has often delivered – that the Fed does not make policy other than on the available information about the economy and market conditions, and only seeks to fulfill the dual mandate of price stability and maximum employment. Fiscal policy he leaves to elected officials.

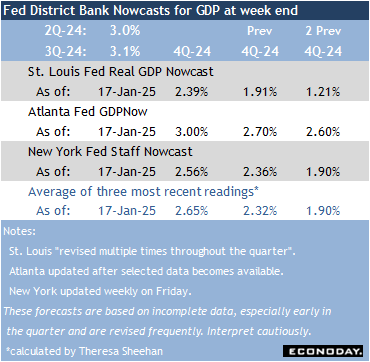

Among the economic data, the advance estimate of fourth quarter 2024 GDP at 8:30 ET on Thursday may be the most interesting item on the calendar. The three district bank GDP Nowcasts are more-or-less in alignment The St. Louis Real GDP Nowcast looks for growth of 2.39 percent and the New York Fed Staff Nowcast is at up 2.56 percent for the quarter. The Atlanta Fed’s GDPNow has the best track record for predicting BEA advance estimate – although it and the other forecasts rarely hit the button. Averaging the three estimates tends to do a bit better and would point to growth in the fourth quarter at around 2.65 percent.

Fed policymakers won’t have the GDP number in hand when they make their decision, but they can certainly find enough data to assess US economic conditions as moderately expansionary and supportive of the labor market. That, along with an uptick in overall inflation and inflation expectations is enough to keep monetary policy on hold for the time being.

—

Originally Posted January 27, 2025 – High points for economic data scheduled for January 27 week

Disclosure: Econoday Inc.

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!