- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 29, 2022 at 3:40 pm

By: Ryan Rasmussen and Gayatri Choudhury

A widespread criticism of crypto is that it has no fundamentals. Skeptics making this argument usually point to bitcoin, which—like gold—does not produce any cash flows.

It’s a fair criticism: While we at Bitwise think bitcoin has a bright future, talking about its “fundamentals” is challenging. But this criticism does not extend to all of crypto.

Most crypto assets have traditional fundamental metrics—revenues, users, user activity, and more. These metrics can be reliably measured and used to evaluate the progress of various crypto protocols and derive potential valuations.

In this column, I review six of the most important fundamental metrics we use at Bitwise to evaluate crypto assets in the Decentralized Finance (DeFi) space. In future columns, my colleagues and I will look at fundamental metrics in other areas of crypto.

Before we get to the metrics, let’s start with a primer on DeFi.

Decentralized Finance (DeFi) refers to a category of crypto-powered applications that have the potential to change how we use financial services. In less than four years, the DeFi ecosystem has grown from zero to more than 2,500 crypto applications that provide financial services like trading, lending, borrowing, and asset management. To date, nearly 5.2 million users have allocated $75 billion to these applications.

The defining feature of these fintech-style applications is that, unlike with all other financial services, no centralized company runs them behind the scenes. Instead, blockchain-hosted software operates the applications automatically based on logic and rules written in their code: No employees, no corporate offices, and no CEOs.

That may sound like science fiction, but it’s not. One example: Uniswap is a DeFi app that lets users trade crypto assets in the same way they can on Coinbase. Last month, Uniswap processed $32.5 billion in trading volume. For comparison, Coinbase processed $47.0 billion.

Impressive, right? Now consider that Coinbase has 4,700 full-time employees while Uniswap has zero.¹

As the DeFi space grows, investors must understand how to evaluate these applications. This column will explore six fundamental metrics for doing just that: Revenue, Profit, Users, Transaction Activity, Committed Capital (or Total Value Locked), and Security.

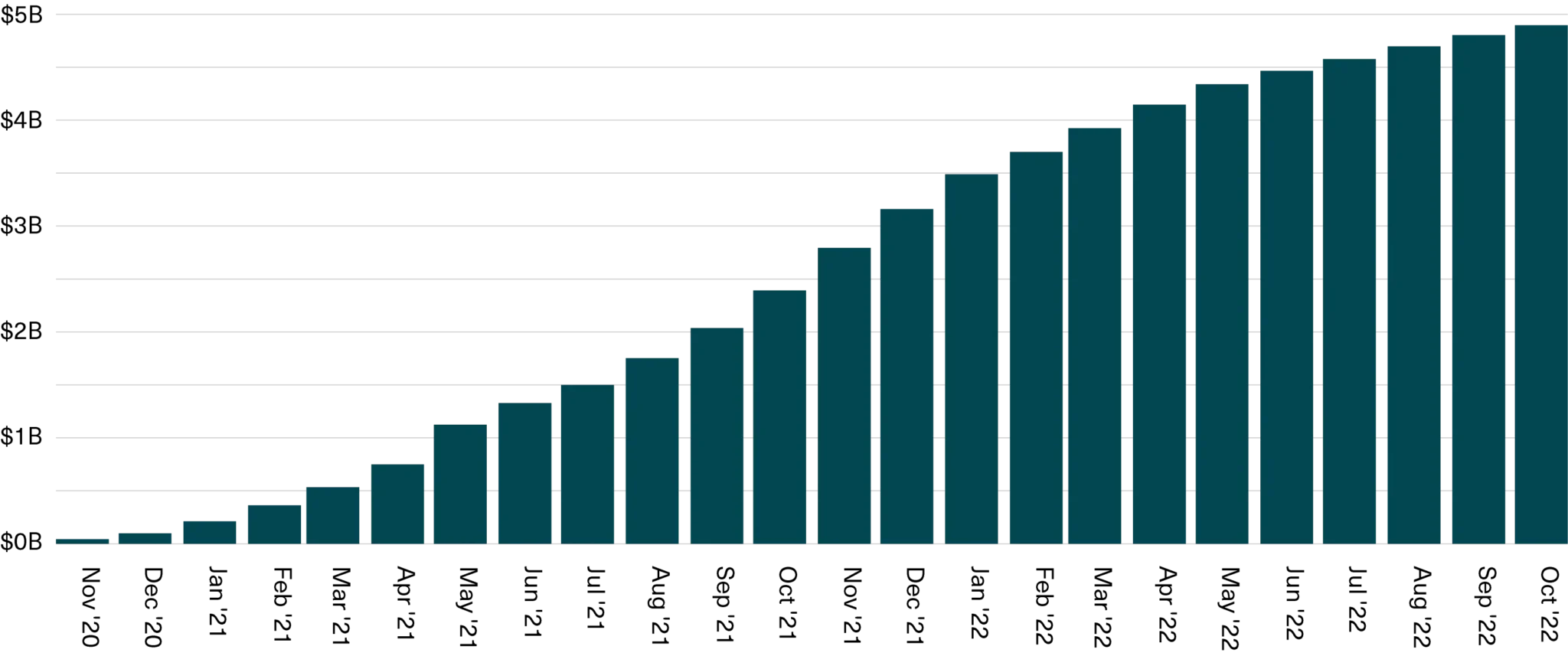

DeFi applications produce revenue, just like traditional financial institutions. In October 2022, for example, the revenue generated by the top ten DeFi applications by market capitalization reached $92 million. Over the past two years, they generated $4.9 billion in revenue.

Cumulative monthly revenue of the leading DeFi applications from November 2020 to October 2022 (USD billions)

Source: Bitwise Asset Management. Data from The Block, CryptoFees.info, and Token Terminal as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index.²

The revenue generally comes from charging users a fee for transacting on the application. For decentralized exchanges like Uniswap, revenue reflects the fees that users pay to access the service (Uniswap charges a 0.3% fee on most trades). Similarly, Aave, a lending application, carves out a portion of the interest revenue borrowers pay and charges a 0.09% fee on “flash loans,” among other revenue streams.

The table below shows the primary source and value of the revenue generated by the leading DeFi applications since 2019. (Many don’t have data for 2019 because they hadn’t launched yet.)

Annual revenue of the leading DeFi applications from January 2019 to October 2022

Source: Bitwise Asset Management. Data from The Block, CryptoFees.info, and Token Terminal as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index and are sorted by market capitalization.² Asterisks indicate that data is not currently available. Dashes indicate that the protocol had not yet launched.

Looking at the table, a few things are clear. For one, these apps generate significant revenue, measuring in the hundreds of millions or billions of dollars per year. For another, revenue is down significantly in 2022 versus 2021—not surprising, given last year’s bull market—but far above 2020 levels.

Importantly, revenue doesn’t equal profit: Just as with companies, there are costs to running DeFi applications. In the case of DeFi, those costs are the portion of revenues paid to individuals that supply capital and liquidity. Additionally, a few applications are already channeling part of their revenue to token holders in the form of dividends or buy-backs, and more are expected to do so in the future.

For instance, of the 0.04% fee that Curve charges users for every trade, half is passed on to liquidity providers and the other half to CRV holders, similar to a dividend. And the Aave lending application uses a portion of profits to buy AAVE tokens on the secondary market and “burn” them (i.e., permanently remove them from circulation), much like a stock buy-back.

However, this isn’t true for all applications. With Uniswap, for example, 100% of the $1.1 billion in user fees the platform generated over the past year was paid to liquidity providers, with no portion accruing to UNI token holders. There is an expectation that that may change in the future, but for now, the platform has no “profit.”

When evaluating DeFi applications, understanding how much profit exists for token holders—and how the profit is distributed—is an important nuance.

Revenue and profit of the leading DeFi applications from November 2021 to October 2022

Source: Bitwise Asset Management. Data from The Block, CryptoFees.info, and Token Terminal as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index and are sorted by market capitalization.² Asterisks indicate that data is not currently available. Note: Profit represents the portion of revenue retained by the protocol.

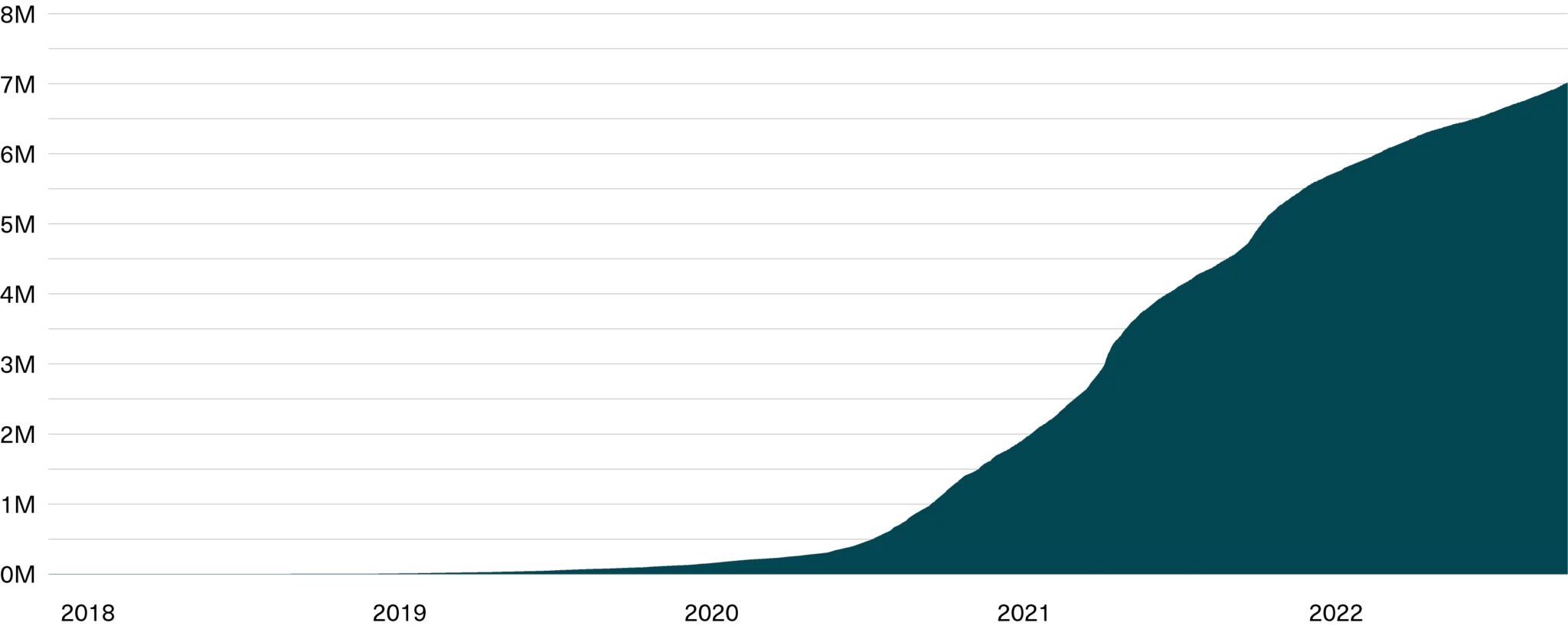

The next fundamental metric for DeFi is “active users”: How many people use these DeFi applications.

Today, DeFi boasts an estimated 7.0 million users, compared to just 0.8 million users two years ago. These users are distributed around the world, with verified DeFi activity taking place in 156 countries.³

Cumulative users in the DeFi ecosystem from January 2018 to October 2022 (millions)

Source: Bitwise Asset Management. Data from Dune Analytics as of October 31, 2022.

We can further parse users by application type.

For decentralized exchanges, which allow anyone to trade crypto assets, users are the liquidity providers looking for yield on their crypto assets and traders willing to pay for access to liquidity. On average, in October 2022, nearly 42,000 users interacted daily with Uniswap (the most prominent decentralized exchange). For lending protocols, users include people who deposit crypto assets in exchange for interest income and those that borrow crypto assets by posting collateral. On average, in October 2022, more than 4,700 users interacted daily with Aave (the largest DeFi lender).

The most noticeable thing when looking at Uniswap and Aave’s active users is that the number of users interacting with Aave daily is roughly 10% of those interacting with Uniswap. That’s not surprising given the nature of the services each application provides—far fewer people are depositing assets and taking loans in a given day than trading.

Still, the trend is positive for both applications.

Cumulative users of the leading DeFi applications from October 2019 to October 2022

Source: Bitwise Asset Management. Data from Token Terminal and Dune Analytics as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index and are sorted by market capitalization.² Asterisks indicate that data is not currently available. Dashes indicate that the protocol had not yet launched.

It’s worth noting that the reported active users of a DeFi application should generally be viewed as an upper-bound estimate rather than an exact measure. That’s because a “DeFi user” represents a unique cryptographic address interacting with a DeFi application. This does not correspond 1:1 with unique users, as one user can control more than one address and vice versa. Still, it gives a good view of the potential health of the ecosystem and how it is evolving over time.

For some DeFi applications, the most relevant metrics are trading or transaction volume, as they provide the most direct measure of the popularity of each service.

Among decentralized exchanges, for instance, Uniswap is the clear leader in terms of trading volume: In October 2022, the application handled $32.5 billion of the $50.8 billion total DeFi trading volume—an impressive 63.9% dominance within the sector.

Annual decentralized exchange (DEX) trading volumes from January 2019 to October 2022

Source: Bitwise Asset Management. Data from The Block and CoinGecko as of October 31, 2022. Dashes indicate that the protocol had not yet launched.

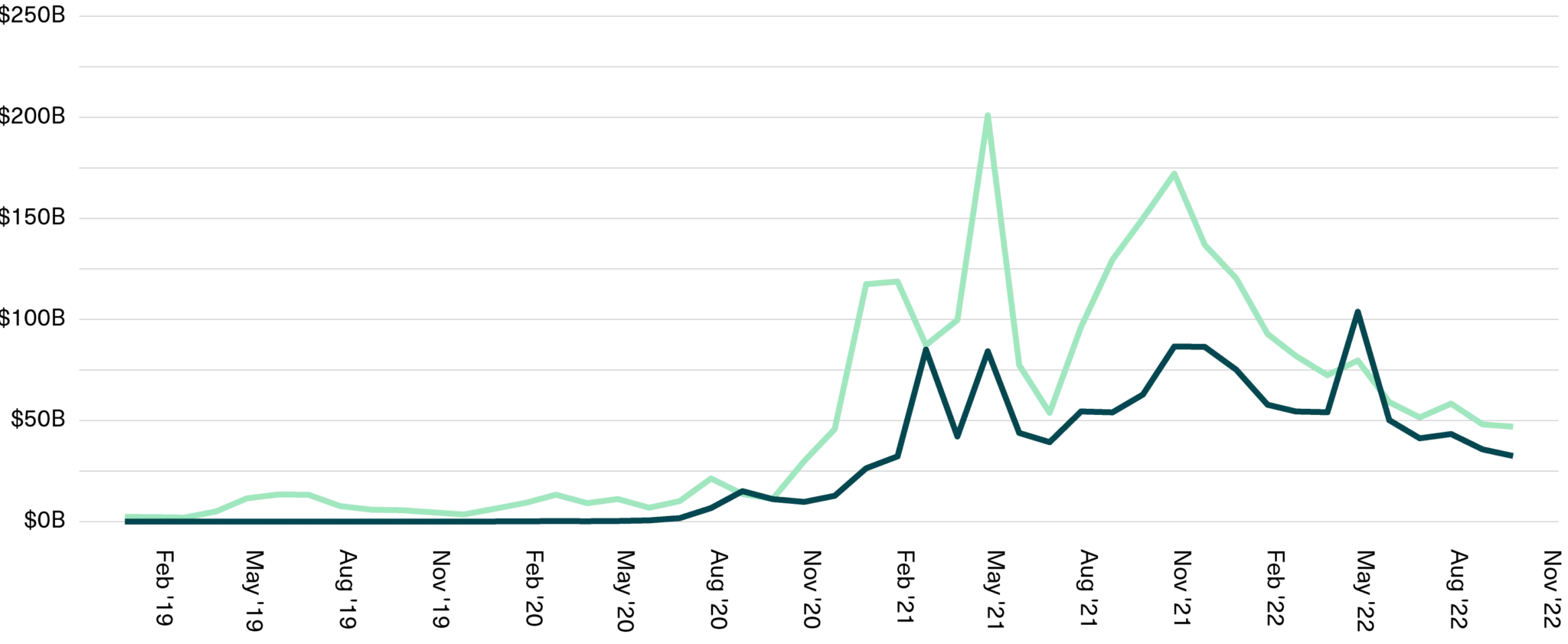

One way to put Uniswap’s trading volume in context is by comparing it to the trading volume of Coinbase, the largest centralized exchange in the U.S. While it’s an oversimplified comparison, it can be a helpful aid in understanding Uniswap’s growth, market share, and potential value.

The chart below illustrates that comparison. Of note, Uniswap currently handles 75% of Coinbase’s trading volume, although its market cap is less than 40% of that of Coinbase.

Trading volume of Uniswap vs. Coinbase from January 2019 to October 2022 (USD billions)

Source: Bitwise Asset Management. Data from The Block, CoinGecko and CryptoCompare as of October 31, 2022.

A similar test can be applied to most DeFi applications and sectors. With stablecoin issuers, for example, one can compare the activity of the stablecoins they issue (e.g., MakerDAO’s Dai or Circle’s USDC). While stablecoin issuers don’t directly earn revenue from activity like sending or trading stablecoins (their revenue primarily comes from earning yield on stablecoin reserves), growing activity is a great indicator of demand and market share trends. For example, the leading crypto-backed stablecoin, Dai, is on track to settle $1.1 trillion in value in 2022; this represents an increase of nearly 850x from 2020 and accounts for 14.4% of all activity among the leading five stablecoins (compared to 0.5% in 2020).⁴

Total activity of the five leading stablecoins from January 2019 to October 2022

Source: Bitwise Asset Management. Data from The Block and Coin Metrics as of October 31, 2022.

One popular metric used to gauge the size of individual DeFi applications and the broader ecosystem is “Total Value Locked,” or TVL. It represents the aggregate amount of capital committed to (or “locked in”) DeFi applications at a particular time. As of October 31, 2022, the TVL across all DeFi platforms has reached $75 billion, having grown 131x since the same time three years ago.

Total value locked (TVL) of the leading DeFi applications from October 2019 to October 2022

Source: Bitwise Asset Management. Data from DeFi Llama as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index and are sorted by market capitalization.² Asterisks indicate that data is not currently available. Dashes indicate that the protocol had not yet launched.

Generally speaking, the more TVL in a DeFi application, the better. With trading applications like Uniswap, for example, TVL is a liquidity measure of the amount of capital committed to the ecosystem by liquidity providers (i.e., market makers). As in traditional markets, traders prefer to use exchanges with more liquidity versus less liquidity, which leads to more trading volume (and more revenue) and in turn attracts more liquidity, fueling the flywheel.

For DeFi lending applications, TVL consists of crypto assets deposited by users that enable them to borrow (or lend) crypto assets and pay (or receive) interest income. For staking applications, TVL consists of the crypto assets deposited by users that allow them to earn staking rewards.

The TVL metric is far from perfect. One issue is that most of the value “locked” in DeFi is denominated in crypto assets like Ethereum, while TVL is often represented in dollars, which means the metric rises and falls with the market. Additionally, DeFi applications may measure TVL differently, and crypto researchers are still improving measurement standards. Still, if not taken too rigidly, it can paint a picture of how the industry has been evolving and growing.

We consider security a key metric in evaluating DeFi protocols. Unfortunately, there have been multiple significant hacks of DeFi protocols over the years. Fortunately, there are ways to assess the security of crypto protocols.

One security element we look at is whether an application’s code has gone through multiple security reviews and audits. For instance, Aave’s latest software upgrade had five code reviews conducted by five security auditing firms before it went live. While they can’t guarantee that a protocol is immune to exploits, code audits are a critical investment in platform security that proactively identify issues and vulnerabilities that developers can address before hackers exploit them.

A second security measure to consider is the number and value of security exploits a protocol has suffered. One noteworthy observation from the table below is that most of the leading DeFi applications have experienced zero hacks or exploits since their launch.

Exploits of the leading DeFi applications since launch

Source: Bitwise Asset Management. Data from DeFi Llama and Messari as of October 31, 2022. Leading DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index and are sorted by market capitalization.²

A third critical measure is simply the age of a protocol: The longer an application has existed and held substantial assets, especially if it has experienced varied market conditions, the more likely it has been tested and found sound. This may be the most intuitive—and important—measure of security.

With growing revenue, users, and capital committed, many DeFi applications resemble—and compare favorably with—high-growth, early-stage equities. Of course, progress isn’t linear: Most applications have seen declining activity in the bear market. Still, the sector has made significant progress in recent years.

Savvy investors can use the fundamental metrics outlined above to track different applications’ progress and build their convictions about individual DeFi assets and the space as a whole.

Still, deriving appropriate valuation targets from fundamentals is complex, subject to assumptions, and must be done individually for each protocol since each has its own particular factors to consider. But that’s not unlike the “valuation challenge” facing venture capital investors who are considering an allocation to early-stage growth companies. And as we’ll see in future columns, DeFi isn’t the only area of crypto where investors can use fundamental metrics to evaluate the trajectories, and potential valuations, of the most important assets.

(1) Coinbase, “Q3 2022 Shareholder Letter,” November 2022, https://s27.q4cdn.com/397450999/files/doc_financials/2022/q3/Q32022-Shareholder-Letter.pdf. Note: There are other entities that contribute to the Uniswap protocol, like Uniswap Labs, that do have employees.

(2) Top DeFi applications are defined as the constituents of the Bitwise Decentralized Finance Crypto Index. The Index identifies the largest investable DeFi assets by market capitalization, subject to eligibility requirements. For the full Index methodology, please visit www.bitwiseinvestments.com/indexes/methodology.

(3) Chainalysis, “The 2022 Geography of Cryptocurrency Report,” October 2022, https://go.chainalysis.com/rs/503-FAP-074/images/2022-Geography-of-Cryptocurrency.pdf

(4) “Stablecoin Activity” refers to Adjusted Transfer Value of Stablecoins (USD), or the USD value of the sum of the stablecoin’s native units transferred, removing noise and certain artifacts. Only non-zero-value, successful transfers with distinct sender and recipient are considered.

—

Originally Posted November 17, 2022 – Six Fundamental Metrics To Evaluate DeFi Assets

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Bitwise Asset Management and is being posted with its permission. The views expressed in this material are solely those of the author and/or Bitwise Asset Management and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!