- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 22, 2021 at 4:10 pm

The article “Climate Change and Asset Allocation” first appeared on Alpha Architect Blog.

This article focuses on “climate-aware” asset allocation and the associated impacts of higher temperatures on equity excess returns and risk. The objective of this research is to demonstrate how portfolios can incorporate climate change risk and rewards into the decision-making process. The research does not comment

The analysis proceeds in two steps:

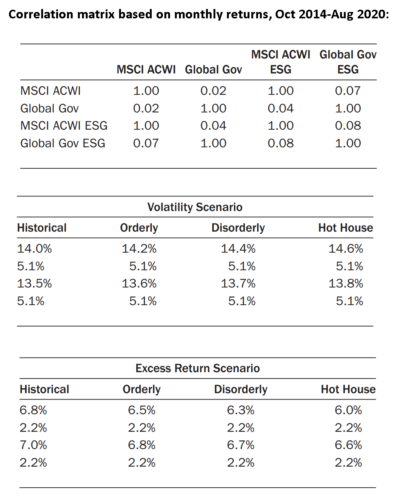

The traditional assets used in the analysis include the MSCI ACWI 1 and the J.P. Morgan Global Government Bond index 2. The ESG assets used include the MSCI ACWI ESG index 3 and the J.P. Morgan Global Government Bond ESG index 4. The cash index for excess returns is the Bloomberg Barclays Short Treasury 1–3 Month Total Return index 5. The observation period includes monthly data from October 2014 through August 2020.

Three climate change scenarios are analyzed and compared to a baseline historical scenario.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

2. The authors use the traditional mean-variance optimization framework which allows the incorporation of constraints and information contained in each of the climate-change scenarios. They include an estimate of the cost of the ESG constraint by adding a shadow price. The shadow price represents the extent to which a relaxation of the constraint will improve the optimization objective of maximizing the Sharpe ratio. In other words, how much of the Sharpe ratio the investor will forgo (cost) if the climate constraint is imposed (benefit of achieving the ESG goal).

For the three climate-change scenarios, the optimized portfolios contained 46% in the Government Bond Index and 0% in the MSCI ACWI equity index. Traversing the historical to the hot house scenario, as shown in Exhibit 6, the allocation to ESG equity index dropped to 30% from 32%, and the allocation to the ESG bond index increased from 22% to 25%. The change in basis points of risk and return is a clear indication of the shadow price of imposing the constraints. Whether or not the costs are “worth it” is a matter of preference.

Although markets are generally thought to be efficient, longer-term risks take a backseat to salient short-term concerns. Climate change is the type of risk/reward opportunity that markets are less likely to price efficiently. In this article and other research, the climate-induced downward pressure on returns and upward pressure on volatility is documented. The authors demonstrate that portfolios constructed without such considerations produce portfolios that are very different from those constrained by climate and temperature change considerations. Adopting a methodology and process that incorporates various scenarios on temperature change possibilities provides an opportunity for investors to assess and balance the consequent patterns of risk and returns.

Visit the Alpha Architect Blog for insight on the most important chart from the paper.

Notes:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!