- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 20, 2021 at 1:00 pm

The post Boards are More Diverse-What about Board Leadership? first appeared on Alpha Architect Blog.

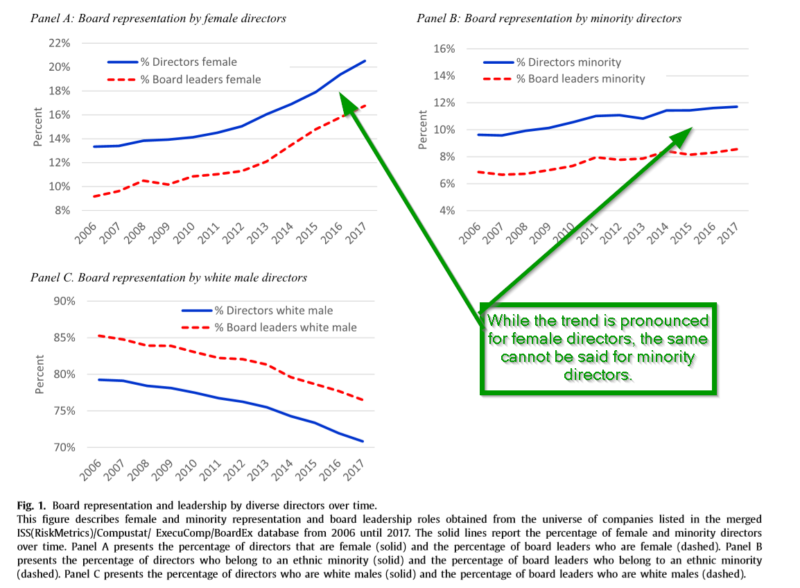

Quite a bit of research has been conducted on the representation of minorities and/or women in the boardroom. However, there is less research on how much diversity there is among board leadership. Board leadership is important because these individuals are responsible for setting the agenda and direction of the board itself. The research under discussion examines the degree to which women and minorities serve in leadership roles. With a large universe of 19,686 individual, nonemployee directors serving on 2,254 unique US corporate boards, the authors are able to examine the complete set of candidates for a specific leadership board position. The extensive nature of the universe permits the comparison of characteristics of directors appointed as board leaders to those that are not so appointed. The article is quite detailed. The major research questions are as follows:

This research raises new questions and issues regarding board inequality. In contrast to most research that documents the paucity of women and minorities appointed to boards of directors, this research points to the presence of a leadership gap even after women and minorities have been appointed to boards in significant numbers. The authors argue that this leadership gap in diversity on corporate boards persists in spite of increasing diversity representation. Despite the evidence that diverse directors exhibit equivalent or superior qualifications, skills, and experience, and perform leadership duties as well as their non-diverse counterparts, appointments to key leadership board positions do not accrue. Simply increasing the percentage of women and minorities in board composition does not do the trick. Without policies that overtly promote diversity and especially including diverse directors on nominating committees, the leadership gap will persist.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

We explore the labor market effects of gender and race by examining board leadership appointments. Prior studies are often limited by observing only hired candidates, whereas the boardroom provides a controlled setting where both hired and unhired candidates are observable. Although diverse (female and minority) board representation has increased, diverse directors are significantly less likely to serve in leadership positions, despite possessing stronger qualifications than non-diverse directors. While specialized skills such as prior leadership or finance experience increase the likelihood of appointment, that likelihood is reduced for diverse directors. Additional tests provide no evidence that diverse directors are less effective.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!